How to Prepare Accurate and Compliant RPIE Statements?

To prepare an accurate and compliant RPIE statement, a CPA works closely with property owners to ensure every detail meets reporting requirements. The process begins with gathering and organizing all financial information, such as income and expense data, rent roll, and utility bills. A skilled CPA ensures that your RPIE statement is both complete and precise, reducing the risk of errors or penalties due to missing or incorrect data. From my experience, the key is timely filing and proper documentation.

Interpreting and Analyzing your RPIE Statements Effectively

A CPA plays a key role in reviewing and analyzing RPIE statements to ensure accuracy and compliance. By carefully examining your financial data, the CPA can identify errors or inconsistencies that might cause incorrect property assessments or inflated tax bills. This process helps maintain accurate reporting while protecting you from costly mistakes that could affect your property’s valuation. From my professional experience, interpreting RPIE statements effectively isn’t just about spotting problems, it’s about discovering opportunities.

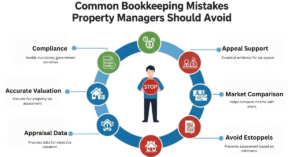

Ensuring Full Compliance with RPIE Filing Regulations

Meeting Filing Requirements

A CPA ensures your RPIE statement meets all regulatory requirements, includes required information, and follows applicable laws to prevent errors or penalties.

Audit and Tax Support

During an RPIE audit, a CPA helps respond to the Department of Finance, ensures fairness, and provides tax planning strategies to reduce liabilities and maximize savings.

Why should every property owner file a RPIE Statement?

Filing an RPIE statement is not just a legal requirement, it’s a smart financial tool for property owners. By analyzing income and expenses tied to their property, owners can identify areas to reduce costs and increase revenue. For instance, if utility costs appear unusually high, the owner can explore energy-efficient options to lower expenses and improve profitability. From my experience, consistent RPIE reviews give property owners a clearer view of their financial health and help in strategic decision-making.

Simple Steps to Create Reliable Financial Statements

Gather Financial Data

Collect invoices, receipts, and bank statements to build an accurate view of your financial performance and identify cost-saving opportunities.

Categorize and Organize

Sort data into revenue, expenses, assets, and liabilities to ensure clarity, smooth reporting, and regulatory compliance.

Draft Core Statements

Prepare your income statement, balance sheet, and cash flow statement to track profitability, assets, and cash flow effectively.

Review and Finalize

Carefully reconcile figures, verify accuracy, and have a CPA review your statements to ensure transparency, integrity, and compliance with accounting standards.

Essential Elements of a Profit and Loss Statement

- Revenue: The total money earned from sales, services, and other income sources before deductions.

- Expenses: All operating and non-operating costs including rent, salaries, utilities, and marketing.

- Gross Profit: What’s left after subtracting the cost of goods sold (COGS) from total revenue.

- Net Profit or Loss: The final amount after all expenses, showing actual profitability.

- Capital Expenses: Major investments like equipment or property upgrades that impact long-term growth.

A Clear Guide to Creating a Profit and Loss Statement

Choose a Reporting Period

Start by deciding the time frame your P&L statement will cover, weekly, monthly, quarterly, or yearly. This helps you track your revenue and expenses consistently and assess performance over time.

Track Revenue and Calculate COGS

Record every source of business income, including sales and services. Then determine your Cost of Goods Sold (COGS) by adding opening inventory to purchases and subtracting ending inventory. This helps identify gross profit accurately.

Record Operating Expenses

List all operating and non-operating costs such as rent, payroll, utilities, marketing, and depreciation. Tracking OpEx ensures compliance with accounting standards and highlights areas for cost reduction.

Calculate Net Profit

Subtract total expenses, interest, and taxes from your gross profit to find your net profit or loss. This reveals your company’s real financial performance and helps plan for future growth.

Smarter Expense Tracking Strategies to Maximize Profitability

Efficient expense tracking is the foundation of a strong RPIE statement and long-term business profitability. Using advanced tools like expense management software helps automate recurring costs, categorize transactions, and keep financial data accurate and transparent. A system like Rippling not only consolidates payroll, benefits, and corporate cards but also offers real-time visibility into your cash flow, helping you stay on top of spending patterns.

- Automate expense tracking to save time and minimize manual errors.

- Use AI-powered tools to categorize transactions accurately.

- Set spending limits with customized approval workflows.

- Monitor cash flow regularly for financial consistency.

- Flag policy violations early to prevent overspending.

Understanding the Purpose and Value of an Income Statement

An income statement, often called a profit and loss statement (P&L), gives a clear picture of your company’s financial performance over a specific reporting period, if it’s a month, quarter, or year. It highlights your revenues and expenses, revealing the net income or net loss your business achieved. Think of it as a simple story of your company’s financial activities, showing how much money you earned, what it cost to earn it, and how much profit or loss you made in the end. The value of an income statement goes beyond basic reporting, it’s a tool for tracking performance, spotting trends, and guiding business decisions.

Core Sections You’ll Find in Every Income Statement

Revenue and Cost of Goods Sold (COGS)

Your revenue shows the total income earned from sales, interest, rentals, or royalties, while COGS tracks direct costs like materials, labor, and production. Subtracting COGS from revenue gives your gross profit, which shows how efficiently your products or services generate income.

Operating Expenses

These include day-to-day costs that keep your business running — from salaries, rent, and utilities to marketing, insurance, and R&D. Controlling these helps maintain profitability without affecting operations.

Non-Operating Items

Here, you list costs not tied to daily operations such as interest expenses, loss on assets, or taxes. Tracking these separately gives a clearer view of operational strength.

Net Income

This is your bottom line, calculated after deducting all expenses, including taxes. It reflects your company’s true profitability and overall financial health, the figure that investors and lenders often look at first.

Practical Steps to Prepare an Accurate Income Statement

Set a Clear Reporting Period

Decide whether your report covers a monthly, quarterly, or yearly timeframe. Shorter periods highlight immediate trends, while longer ones reveal long-term growth patterns and strategic insights.

Calculate Revenue and COGS

Add up all income sources, sales, services, or other streams, and subtract the cost of goods sold (COGS) such as materials, labor, or production costs to determine your gross profit.

Record Operating Expenses

List indirect costs like rent, utilities, insurance, or legal fees. These operating expenses (OPEX) show what it takes to keep your business running smoothly beyond production costs.

Compute Final Income and Taxes

Subtract all expenses from gross profit to get your pre-tax income. Then include tax liabilities, local, state, and federal, along with any interest charges, giving a complete and compliant view of your profitability.

| Step | Action | Purpose | Outcome |

| Gather Financial Data | Collect all revenue, expense, and cost records | Ensures completeness of information | Accurate financial base |

| Categorize Transactions | Separate income, operating, and non-operating expenses | Helps in clear financial organization | Easy-to-read statement |

| Calculate Totals | Subtract total expenses from total revenue | Determines profit or loss | Shows true business performance |

| Review & Verify | Cross-check figures and supporting documents | Avoids errors and misstatements | Reliable and audit-ready statement |

Expert Tips for Preparing and using Income Statements Effectively

- Use trusted accounting software like QuickBooks, Xero, or Zoho Books to automate data entry and improve accuracy.

- Keep accurate records of all income and expenses for better tax compliance and decision-making.

- Consult a qualified accountant or financial advisor to interpret data correctly and identify growth opportunities.

- Develop a strong financial strategy using clear insights from your income statements.

- Review regularly to spot patterns, optimize performance, and ensure ongoing reporting accuracy.

Get Professional CPA help to Prepare accurate Income Statements

Working with a CPA gives you more than just precise income statements — it helps you truly understand your business financials. A certified professional accountant brings expertise in analyzing reporting periods, identifying financial trends, and ensuring every entry reflects your company’s real performance. Whether it’s short-term adjustments or long-term strategy, a CPA ensures accuracy and compliance at every step. With professional accounting guidance, you gain clarity and control over your financial reports.