Need a CPA letter fast? We prepare licensed, AICPA-compliant CPA letters for mortgage lenders, landlords, banks, visa officers, and courts — delivered in 2 hours.

Trusted by mortgage brokers, banks, landlords, and immigration attorneys across the United States

A CPA letter — also called a comfort letter, third-party verification letter, or CPA income verification letter — is a formal document prepared by a licensed Certified Public Accountant that verifies specific financial facts about an individual or business.

It confirms income, self-employment status, business existence, tax filing history, or use of business funds — based strictly on tax returns, financial statements, and bank records reviewed by the CPA.

These limits follow AICPA professional standards for third-party verification

A CPA letter is required in many situations beyond mortgage applications. Here are the most common cases where lenders, landlords, and institutions request one.

Verify self-employment income and business stability for lenders.

Confirm income for landlords when you lack traditional pay stubs.

Validate business compliance and financial health for lenders.

Proof of income and employment status for USCIS and embassies.

Income verification for divorce, child support, and bankruptcy cases.

Confirm financials for investors and business partners quickly.

Income and business verification for commercial policy underwriting.

All 12 types issued on official CPA letterhead by Tim Martin, licensed CPA, following AICPA standards.

Confirms income from tax returns and P&L

Third-party verification for mortgage brokers

Fannie Mae / Freddie Mac aligned format

Confirms business expense ratio from financials

Self-employment status and income verification

Income proof for landlords and property managers

Verifies withdrawals won't harm business health

General verification for banks and insurers

Addresses lender questions about income gaps

All types available with notary seal added

Income verification for 1099 and consultants

Confirms business is active and compliant

Not sure which type you need?

A properly prepared CPA letter follows a standard professional format. Here is what every Ignition Tax CPA letter includes:

CPA firm name, address, license number, and contact details

Date of preparation and unique reference for tracking

Lender name, address, and loan reference number

Confirms the client authorized the CPA to release information

Income, employment, business existence, or fund use confirmed

States letter is based on limited scope — not an audit

Personally signed by Tim Martin, CPA

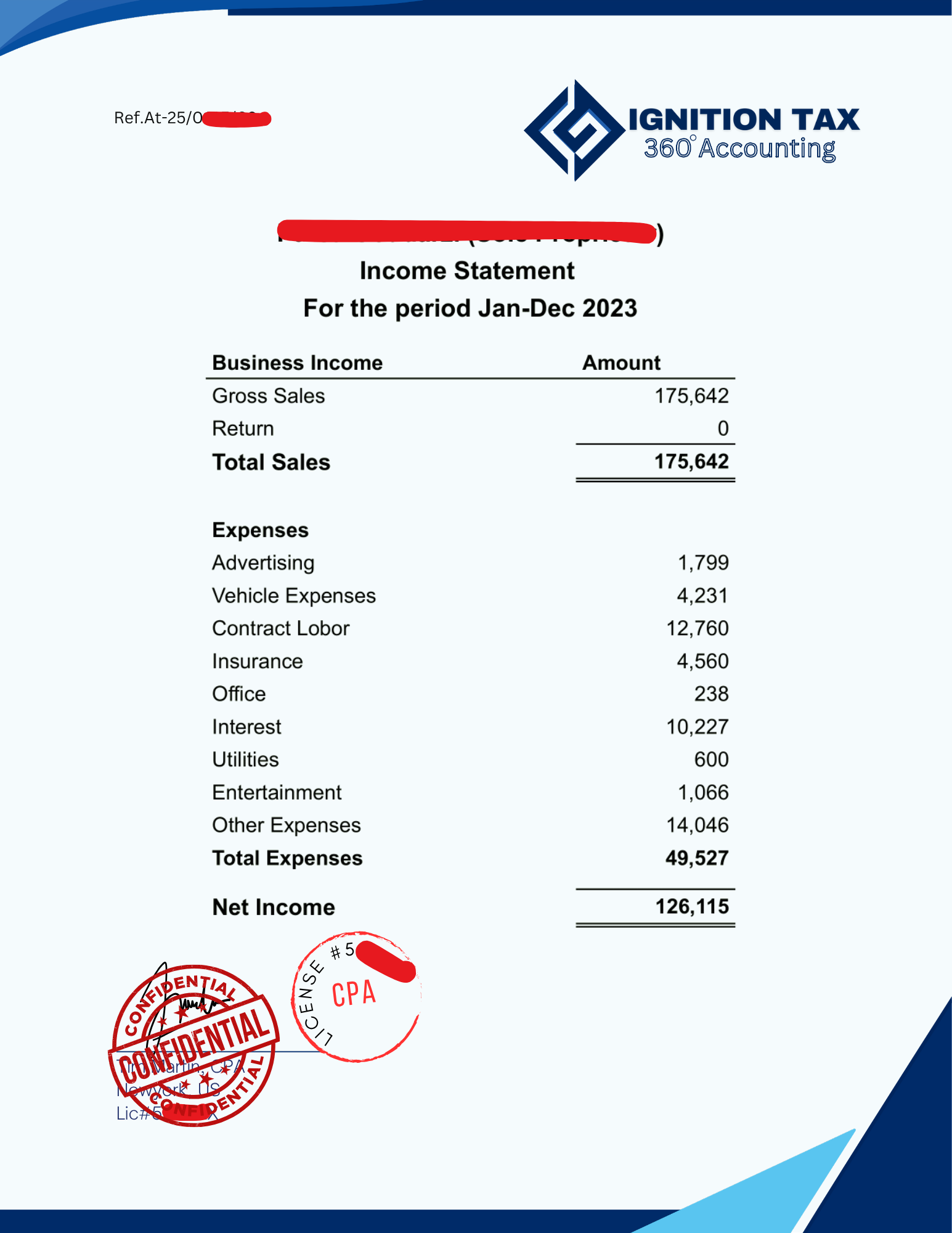

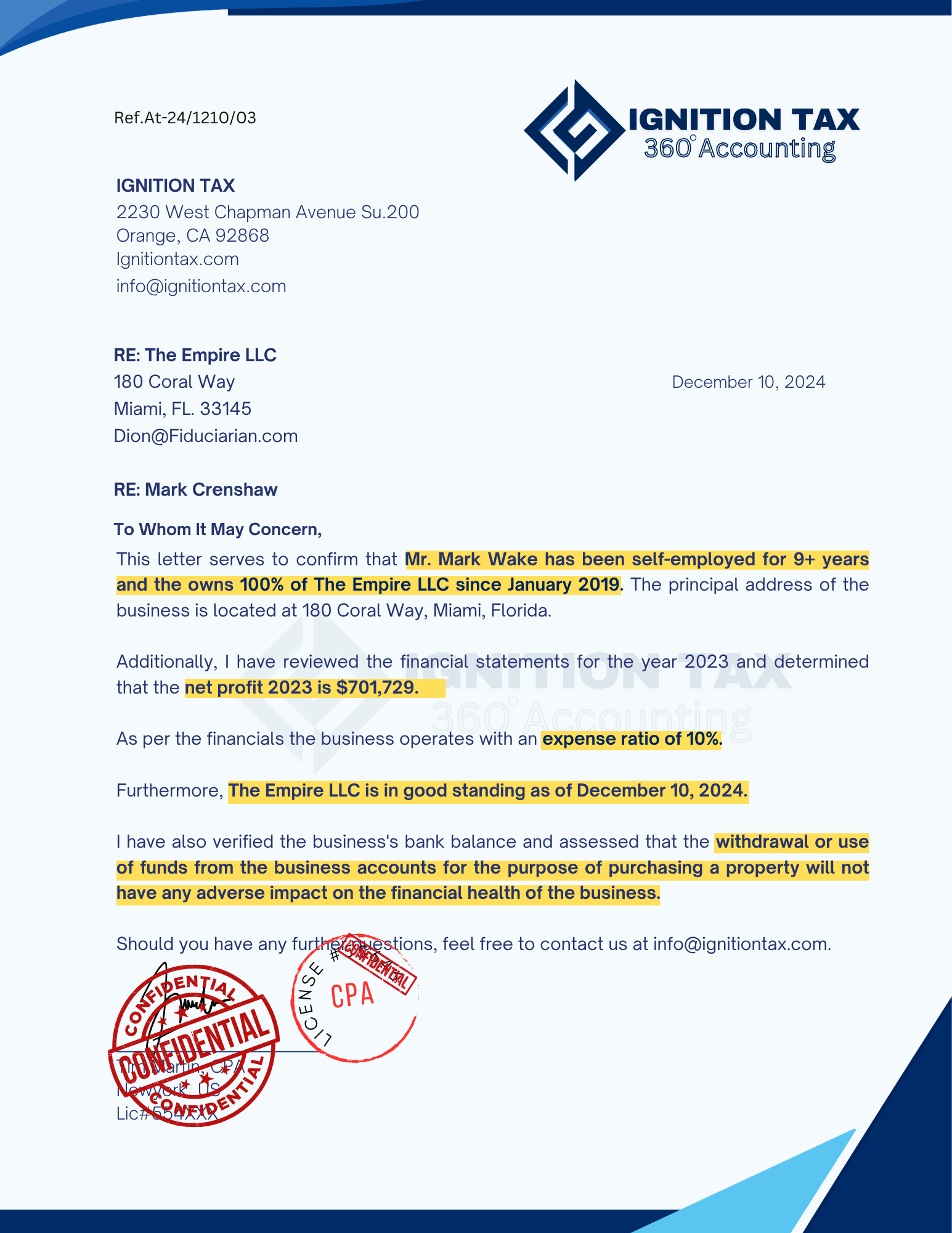

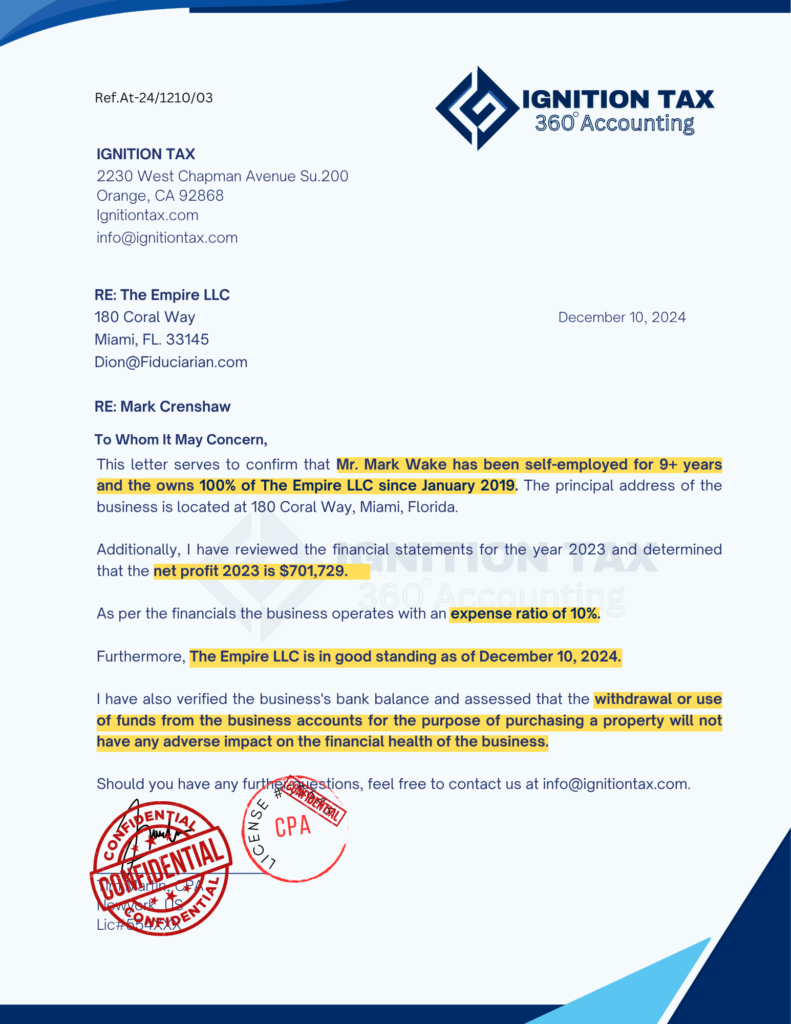

Sample Ignition Tax CPA letter — format follows AICPA professional standards

Most commonly needed by people who cannot provide traditional W-2 forms or pay stubs.

Sole proprietors and LLC owners verifying income from tax returns and financials.

Gig workers aggregating multiple income streams for lenders and landlords.

S-Corp, LLC, and partnership owners confirming income and business health.

Rental income earners needing Schedule E verification for lenders.

Doctors, attorneys, and consultants with K-1 or partnership income.

Whatever your income type — we prepare your letter to match your lender requirements.

Fully remote process. No appointment needed.

Place order online. Select letter type and name your lender. $199 flat fee.

Upload tax returns, P&L, bank statements. We send a clear checklist.

Tim Martin, CPA, reviews and verifies all facts per AICPA standards.

We draft, share for review, sign and stamp on official CPA letterhead.

Letter delivered directly to your lender, landlord, or agency via secure email.

How a CPA letter compares to tax returns, bank statements, and pay stubs.

Every Ignition Tax CPA letter follows this exact format. Client name, financials, and reference numbers redacted for privacy.

Sample Ignition Tax CPA letter — format follows AICPA professional standards. Every letter customized to your specific lender requirements.

Flat fee pricing. You see the full cost before we start.

CPA Letter for Self Employed or Business owners needs a CPA letter for mortgage lender

CPA Letter Plus for Business Partners, Self Employed Individuals need a CPA letter with Notarization

Licensed Certified Public Accountant

Tim Martin holds an active CPA license. License number visible on every letter — lenders can verify it directly with the state board.

Every letter follows AICPA professional standards. Scope, procedures, and limitations clearly stated — no overreach, no liability risk to you.

CPA letters supporting successful mortgage, rental, SBA loan, and visa applications across all 50 US states. Real results, real clients.

If your lender requests revisions, we revise at no charge. If we cannot satisfy your lender's requirements with complete documentation, we provide a full refund.

NY State License

Professional Compliance

Tax Return Verified

All 50 States

Available — $349

We are currently in the process of obtaining a mortgage loan, and the lender requires a CPA letter to verify the following details:

Our lenders require a letter that verifies the business expense ratio, which is 15%. Additionally, the letter should state that “the use of business funds does not have any adverse impact on the business”.

We are currently in the process of fulfilling a request for our tenant, who requires a letter to verify the following details for housing purposes:

— Based on 13 client reviews

As a self-employed person, I needed a CPA letter for my loan. Ignition Tax provided a professional, detailed letter that met all the lender’s requirements. The team was courteous, and everything was done right. Highly satisfied

My biggest concern was getting the CPA letter in time for my mortgage deadline. Ignition Tax delivered it within 2 hours, and I was amazed at how seamless and fast the process was. Highly satisfied

At first, I was a bit confused, but I’m so glad I chose Ignition Tax! The lender accepted the letter without any additional requests. Thank you for making this so easy!

I needed a CPA letter quickly for my mortgage, and Ignition Tax delivered it professionally in no time. Literally, I received it within 2 hours, and the fast turnaround made the entire process so much smoother. I’m happy with the service

I was looking for a verified CPA for my mortgage and found Ignition Tax. They made the process easy and delivered exactly what I needed. I highly recommend their services.

We are a trusted mortgage loan firm and always recommend our clients get their CPA letters from Ignition Tax. They understand exactly what lenders require and deliver accurate, professional documents.

Local service. Remote coverage nationwide.

A CPA letter — also called a comfort letter or third-party verification letter — is a formal document prepared by a licensed CPA that verifies specific financial facts: income, self-employment status, business existence, or use of business funds. It is required by mortgage lenders, landlords, banks, and immigration authorities for individuals who cannot provide traditional W-2 or pay stub documentation.

Ignition Tax charges a flat fee of $199 for a standard CPA letter. Fast delivery in 2 hours. Notarized letters start at $349. Unlike hourly CPA billing at $150–$400 per hour, our flat fee covers document review, letter preparation, revisions, and direct delivery to your lender or landlord — no surprises.

No. A CPA letter must be prepared and signed by a licensed Certified Public Accountant. Self-prepared income letters are not accepted by mortgage lenders, banks, or immigration authorities because they lack third-party verification. The letter must appear on official CPA letterhead with a valid CPA license number.

Only a licensed Certified Public Accountant (CPA) can prepare and sign a CPA letter. The CPA must hold an active state license and follow AICPA professional standards. Accountants without CPA designation, bookkeepers, and enrolled agents typically cannot provide CPA letters accepted by mortgage lenders.

Ignition Tax provides fast delivery is available in 2 hours for urgent mortgage closings, same-day visa appointments, or immediate lease requirements. Submit your order and documents before 12PM EST for same-day processing.

Standard documents: signed federal tax returns for the most recent 1–2 years, a current profit and loss (P&L) statement, bank statements if required by your lender, and your lender or landlord checklist. We provide a complete document checklist immediately after you place your order.

Yes — these terms are used interchangeably in the industry. A comfort letter, third-party verification letter, and CPA income verification letter all refer to the same type of document. The specific name used depends on the lender or institution requesting it. Ignition Tax prepares all variations under the same standard process.

Most mortgage lenders, landlords, and banks do not require notarization. However, some institutions — particularly for visa applications, court proceedings, or international use — may request a notarized CPA letter. Ignition Tax offers notarization on all letter types as an add-on service for $349.

If your lender requests revisions or rejects the letter for professional standard reasons, Ignition Tax will revise it at no additional charge. We maintain a 100% acceptance rate on letters prepared with complete and accurate documentation. If we cannot resolve the issue, we provide a full refund.

Yes — in some cases. If tax returns are unavailable, we can prepare a CPA letter based on available financial records including bank statements, P&L statements, and business records. However, most mortgage lenders specifically require tax return-based verification. We will advise you on what your specific lender will accept.

Most lenders accept a CPA letter dated within 60–120 days of the loan closing or application. Specific validity periods vary by lender and institution. We recommend requesting your CPA letter no more than 60 days before your closing date to ensure it falls within your lender’s acceptable date range.

A CPA letter is a limited-scope document that verifies specific facts from existing records — it does not constitute an audit, review, or compilation. An audit involves independent verification of financial statements and takes weeks to complete. A CPA letter can be prepared in 2 – 24 hours and is specifically designed for third-party income and status verification.

Still have questions?

Step-by-step process guide

Real format with labeled components

Fannie Mae, FHA, Freddie Mac

Full document comparison guide

Full pricing breakdown and comparison

Fast delivery process and requirements

Complete guide for LLC owners

Complete checklist by letter type

Licensed, AICPA-compliant CPA letters for mortgage, rental, visa, and business loan applications — delivered in 2 hours. Flat fee. No surprises. 100% acceptance guarantee.

Need it today? Order before 12PM EST for same-day processing.