A CPA expense ratio letter is a formal document issued by a licensed Certified Public Accountant on official CPA letterhead that confirms the operating expense percentage of a self-employed borrower’s business. The letter states the specific percentage of gross business revenue consumed by operating expenses — derived from the CPA’s review of the borrower’s tax returns, profit and loss (P&L) statements, financial records, and bank statements. It is specifically used by mortgage lenders and underwriters during non-QM bank statement loan evaluations to calculate the borrower’s net qualifying income.

When a self-employed borrower applies for a bank statement mortgage or non-QM loan, lenders calculate qualifying income by deducting business expenses from gross bank statement deposits. Without a CPA expense ratio letter, most lenders automatically apply a default expense factor — typically 50% — regardless of the borrower’s actual business expenses. For a business operating at a 15% or 20% expense ratio, this default cuts qualifying income by 30–35 percentage points, directly reducing the loan amount the borrower qualifies for.

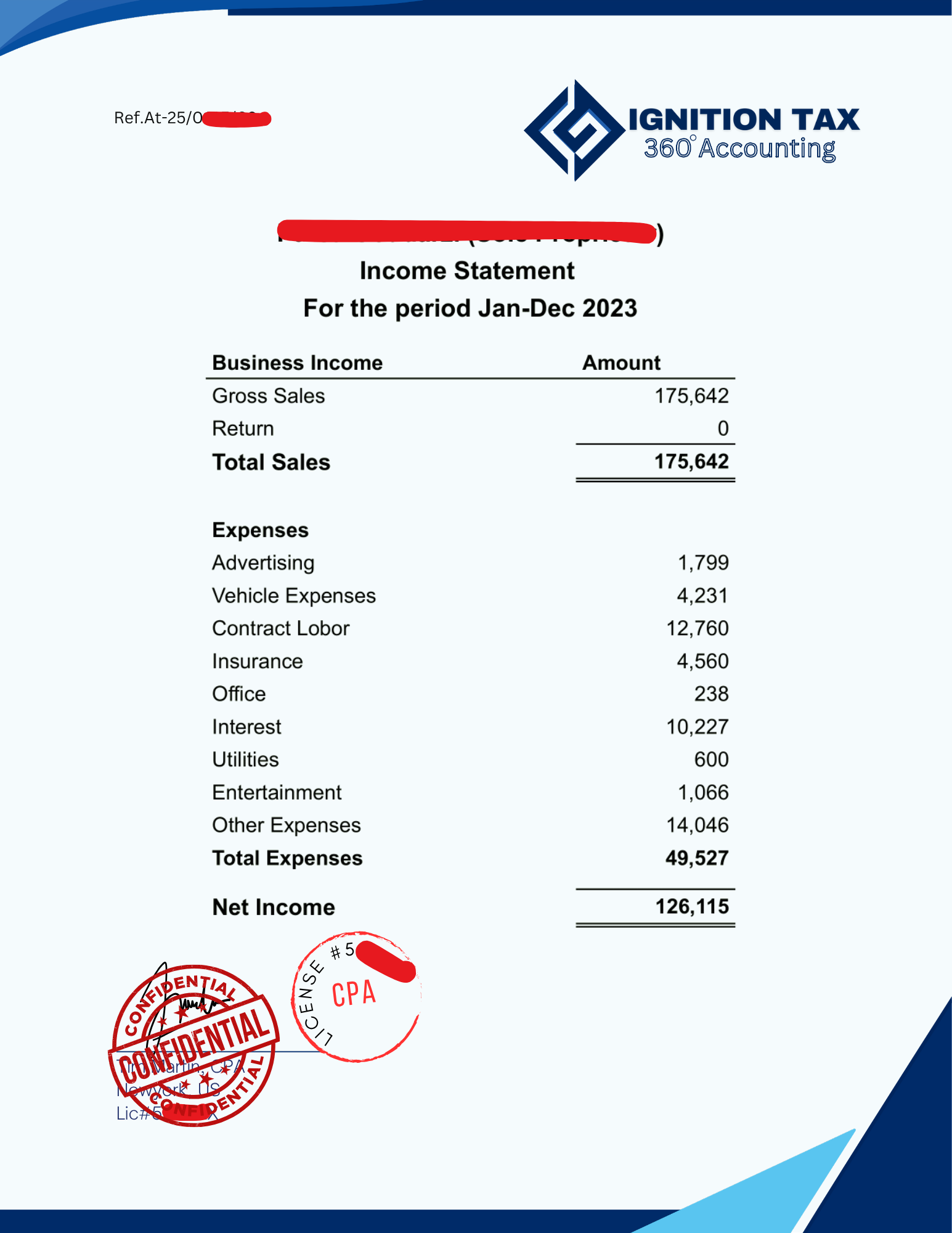

The expense ratio is calculated as total operating expenses divided by gross revenue, expressed as a percentage. A business with $200,000 in gross revenue and $30,000 in operating expenses has a 15% expense ratio. A CPA reviews the business’s financial records — including IRS-filed tax returns, profit and loss statements, and bank statements — and issues a formal letter confirming this verified percentage to the lender or underwriter.

Every Ignition Tax CPA expense ratio letter is personally prepared and signed by Tim Martin, CPA — licensed in New York State, AICPA member — based on a thorough review of your business financial records, written to your lender’s specific requirements, and delivered directly to your underwriter in 2 hours.

Lender’s default expense ratio

Expense deduction

= $4,500 more qualifying income per month

Direct impact on maximum loan amount and DTI ratio

Underwriters aggregate gross business bank deposits, then deduct your CPA-verified expense percentage to establish net monthly income for debt-to-income (DTI) calculation. Without your verified ratio, lenders apply the 50% default — regardless of your actual business costs.

Most bank statement and non-QM mortgage programs establish a default expense factor of 50% — applied automatically when no CPA-verified ratio is provided. Some programs set minimum floors at 20% regardless of the CPA's verified figure. A CPA expense ratio letter prevents the lender from applying an arbitrary default.Most bank statement and non-QM mortgage programs establish a default expense factor of 50% — applied automatically when no CPA-verified ratio is provided. Some programs set minimum floors at 20% regardless of the CPA's verified figure. A CPA expense ratio letter prevents the lender from applying an arbitrary default.

A lower verified expense ratio (e.g., 15% to 30%) increases net qualifying income, improving the debt-to-income (DTI) ratio — enabling qualification for larger loan amounts. For borrowers near the DTI threshold, a CPA expense ratio letter can be the difference between loan approval and denial.

Lenders often have minimum allowable expense ratios — typically 15% to 20% — that the CPA must verify the borrower actually operates above. The letter must confirm the business genuinely operates at the stated expense ratio based on reviewed financial records, not an estimate.

Ignition Tax prepares expense ratio letters written to your specific lender’s exact threshold requirements — ensuring compliance without understating or overstating your actual business expenses. $199 flat fee.

Message us your business type and lender requirements — we confirm the appropriate expense ratio documentation before you order.

The CPA's formal firm name, active state license number, and verified office address — confirming the letter originates from a licensed CPA whose credentials lenders can independently verify with the state licensing board

Business name, legal structure, ownership percentage, and the precise 12-to-24-month lookback period analyzed — explicitly stating the period of bank statements or financial records reviewed

The specific operating expense percentage — defined as total operating expenses (including Cost of Goods Sold) as a fixed percentage relative to gross revenue. This is the primary number the underwriter uses to calculate net qualifying income

Identifies the source records used: filed IRS tax returns, profit and loss (P&L) statements, ledger books, or bank statements — confirming the expense ratio is based on reviewed financial data, not an estimate

When applicable — a statement that the use of business funds for a property purchase or down payment will not adversely disrupt core business operations. Required by Fannie Mae and Freddie Mac for business fund use cases

Personally signed by Tim Martin, CPA — NY State license number on every letter. Not outsourced, not AI-generated, not delegated to unlicensed staff

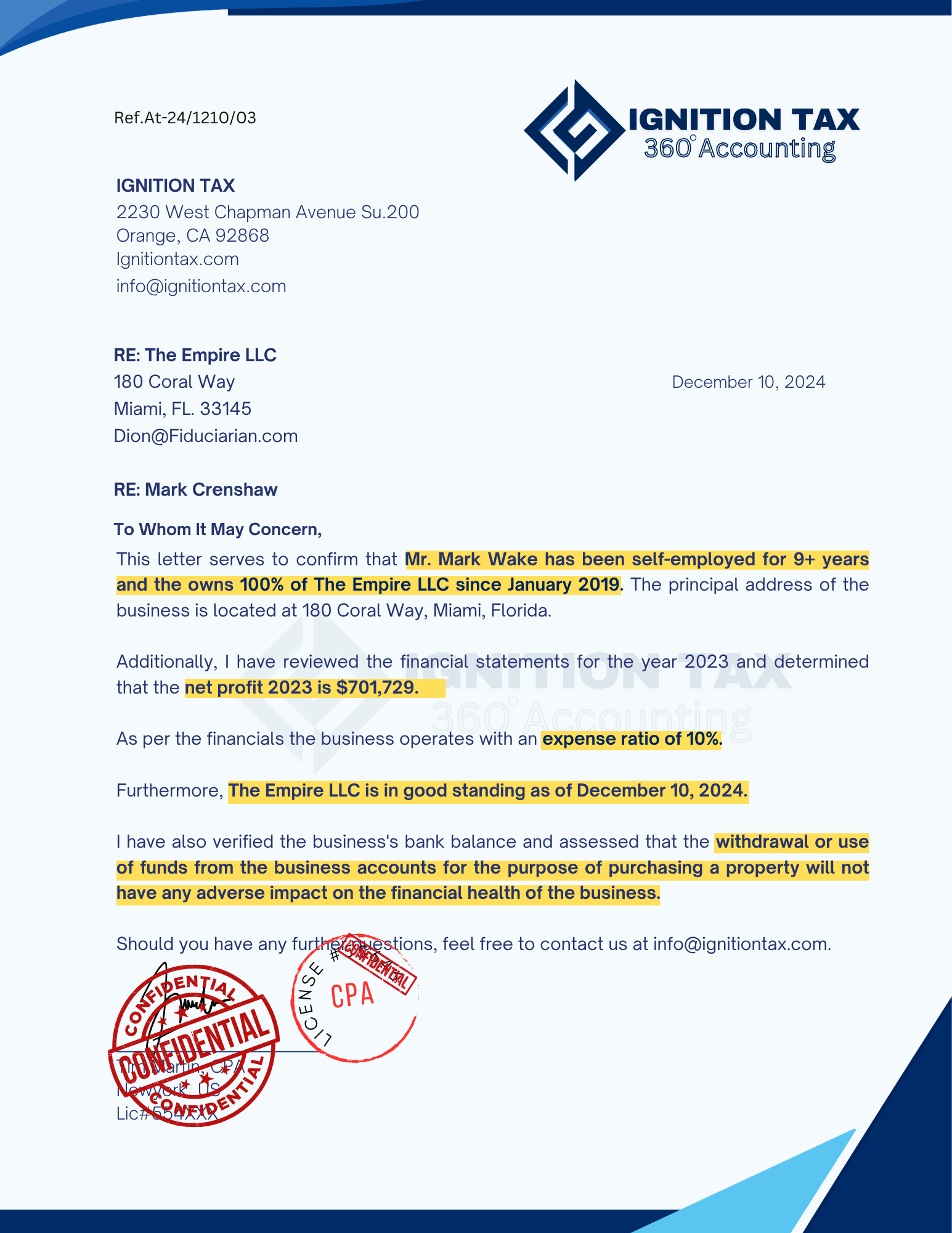

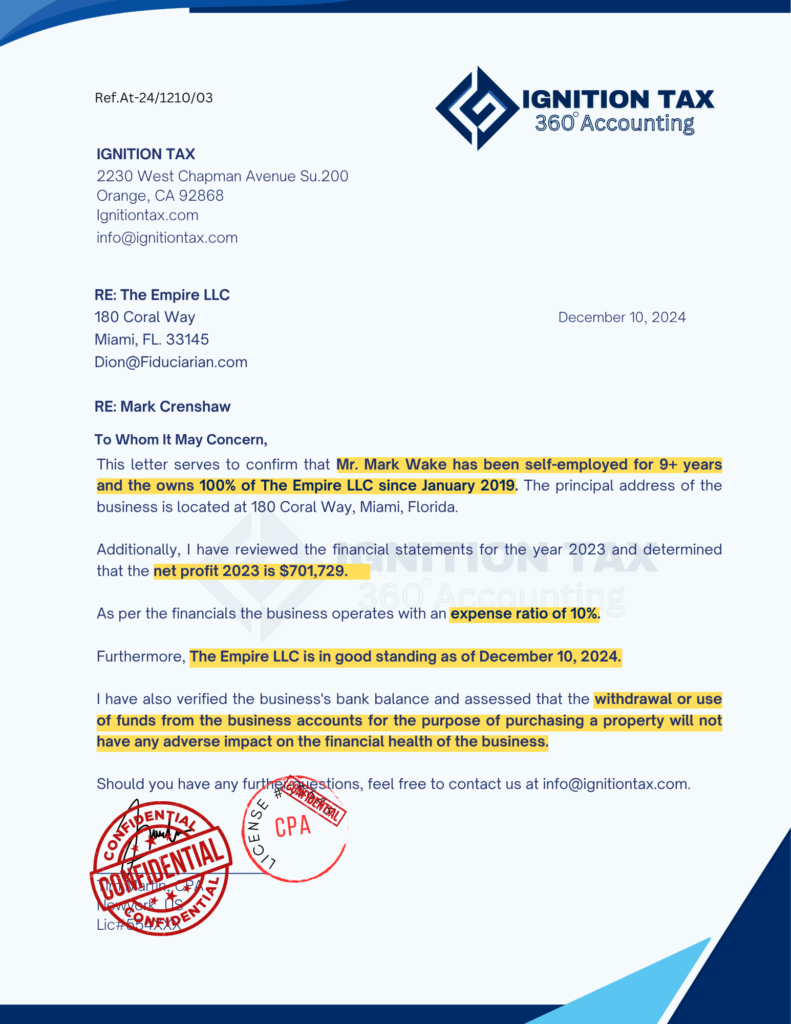

Sample Ignition Tax CPA letter — format follows AICPA professional standards

The primary use case. Bank statement mortgage programs qualify self-employed borrowers based on gross bank deposits — then deduct a lender-determined expense factor to calculate net qualifying income. Without a CPA expense ratio letter, lenders apply the default 50%. A CPA letter replaces this with your actual verified percentage.

Fannie Mae and Freddie Mac require a CPA letter when a self-employed borrower uses business account funds for a mortgage down payment. The letter must confirm both the business's expense ratio and financial health, AND that the fund withdrawal will not adversely impact business operations.

Self-employed borrowers in low-overhead industries — consulting, professional services, technology — may show high revenue but low net profit on tax returns due to deductions. A CPA expense ratio letter explains the discrepancy by confirming actual expense percentages from reviewed financial records.

SBA lenders and business financing institutions request an expense ratio letter as part of their financial health assessment — confirming the business operates with a financially sustainable expense structure relative to gross revenue.

Message us your specific loan situation — we confirm whether an expense ratio letter is the right document before you order.

Every letter is written to your lender’s specific expense ratio threshold. We confirm your lender’s minimum floor percentage before preparing the letter — ensuring full compliance without overstating or understating your actual business expenses.

Select expense ratio letter at $199. Provide your lender's name, their minimum expense ratio floor (15%? 20%?), and the lookback period they require (12 or 24 months).

Upload tax returns (1–2 years), P&L statement, 12–24 months of business bank statements, and your lender's documentation checklist. Bank statements are critical for expense ratio letters.

Tim Martin personally reviews all records, calculates the actual expense ratio from reviewed documents, and prepares a letter stating the verified percentage to your lender's exact threshold. Not estimated — calculated from IRS returns and P&L.

We prepare the expense ratio letter on official CPA letterhead, share a draft for review, adjust threshold language if needed, then sign and stamp with Tim Martin's active NY State CPA license.

Signed letter delivered directly to your mortgage lender or underwriter via secure email — or to you for forwarding. Notarization available for $349.

We are currently in the process of obtaining a mortgage loan, and the lender requires a CPA letter to verify the following details:

Our lenders require a letter that verifies the business expense ratio, which is 15%. Additionally, the letter should state that “the use of business funds does not have any adverse impact on the business”.

We are currently in the process of fulfilling a request for our tenant, who requires a letter to verify the following details for housing purposes:

CPA Letter for Self Employed or Business owners needs a CPA letter for mortgage lender

CPA Letter Plus for Business Partners, Self Employed Individuals need a CPA letter with Notarization

Licensed Certified Public Accountant

Only a licensed Certified Public Accountant can prepare an expense ratio letter accepted by mortgage lenders, Fannie Mae, Freddie Mac, and non-QM underwriters. Tim Martin holds an active NY State CPA license — verifiable with the New York State Board of Regents before the lender even reads the letter.

Underwriting guidelines require expense ratio letters to comply with AICPA professional standards — specifically the prohibition on guaranteeing solvency or confirming ratios without reviewed financial records. Every Ignition Tax expense ratio letter includes the required scope and limitations statement — protecting you and the lender from professional standard violations.

Expense ratio letters supporting successful non-QM bank statement, conventional, FHA, VA, jumbo, and SBA loan approvals across all self-employment income types and all 50 US states.

If your underwriter requests revisions to the expense ratio wording or threshold language, we revise at no charge. Full refund if we cannot satisfy your lender's requirements with complete documentation.

NY State License

Professional Compliance

Tax Return Verified

All 50 States

Available — $349

Everything you need to know before ordering your CPA income verification letter.

A CPA expense ratio letter is a formal document issued by a licensed Certified Public Accountant on official letterhead that confirms the operating expense percentage of a self-employed borrower’s business. The letter verifies what percentage of gross business revenue is consumed by operating expenses — derived from the CPA’s review of IRS tax returns, profit and loss statements, and bank records. Mortgage lenders use this document specifically for non-QM bank statement loans to calculate net qualifying income.

Without a CPA expense ratio letter, bank statement and non-QM mortgage lenders automatically apply a default 50% expense factor — regardless of the borrower’s actual business expenses. For a borrower depositing $15,000 per month, this default produces $7,500 in qualifying income. A CPA-verified 20% expense ratio produces $12,000 in qualifying income — a $4,500 monthly difference that directly affects maximum loan amount and DTI ratio.

Ignition Tax charges $199 for a standard CPA expense ratio letter delivered in 2 hours. A notarized version is $349. ConceptsCPA.com reports that CPA expense ratio letters typically cost $250–$490. Ignition Tax charges $51 to $291 less than typical market rates — with AICPA-compliant wording, a licensed CPA signature, and direct delivery to your underwriter included at no extra charge.

The appropriate expense ratio depends on your actual business financials and your lender’s program requirements. Most non-QM bank statement programs require a minimum expense ratio of 15–20% — even if your actual ratio is lower. A CPA expense ratio letter confirms your actual verified percentage; if it is below the lender’s minimum floor, the lender applies their minimum floor instead. Tim Martin, CPA can review your financials and determine the appropriate documented ratio before you order — message us on WhatsApp at no charge.

No — they serve different purposes. A comfort letter (or CPA income verification letter) confirms self-employment status, income, and business ownership for general third-party verification. A CPA expense ratio letter specifically confirms the precise percentage of gross business revenue used for operating expenses — used in bank statement and non-QM loan underwriting to calculate net qualifying income. Some lenders request both letters for the same loan application.

Ignition Tax delivers standard expense ratio letters in 24 hours when all documents are submitted. Fast delivery is available in 2 hours for urgent closing deadlines — submit your order and all documents before 12PM EST. Expense ratio letters require bank statements in addition to tax returns and P&L statements, so ensure all financial records are ready before ordering to maximize delivery speed.

Required documents: signed federal tax returns (most recent 1–2 years), current profit and loss (P&L) statement, 12–24 months of business bank statements (the lookback period your lender specifies), and your lender’s specific checklist or threshold requirements. After placing your order, Ignition Tax sends a complete tailored document checklist immediately — covering exactly what your specific lender’s program requires.

Conventional mortgages following Fannie Mae and Freddie Mac guidelines do not typically require expense ratio letters — they calculate income from tax returns. CPA expense ratio letters are specifically used for non-QM bank statement programs, some jumbo loan programs, and SBA financing where lenders qualify income from bank deposits rather than tax returns. If your lender has specifically requested an expense ratio letter, your loan is likely a non-QM or bank statement product.

If you change lenders during the loan process, a new expense ratio letter addressed to the new lender may be required — since the letter is addressed directly to the specific institution. However, if the financial data and lookback period remain the same, a revision can often be made at minimal or no additional charge. Ignition Tax includes one revision at no charge with every standard expense ratio letter order.

Rejections are rare when the letter is prepared with the lender’s exact threshold requirements and reviewed financial records. The most common causes of rejection are: (1) the stated expense ratio is below the lender’s minimum floor without explanation, (2) the lookback period does not match the lender’s program requirements, or (3) the data sourcing statement does not clearly identify the financial records reviewed. Ignition Tax maintains a 100% acceptance rate — if your lender requests revisions, we revise at no charge.

Still have questions?

Related CPA letters that self-employed borrowers commonly need alongside an expense ratio letter.

Income verification and comfort letters for mortgage underwriters — Fannie Mae aligned

Confirms business fund withdrawal for down payment won't harm business health

Income verification from tax returns and P&L for lenders and landlords

Self-employment status and income verification — all loan types and use cases

Third-party verification letter for mortgage brokers and lenders nationwide

See all 12 types of CPA letters we prepare for self-employed individuals

Licensed, AICPA-compliant CPA expense ratio letters for self-employed borrowers applying for non-QM bank statement loans, conventional mortgages, and SBA financing — prepared by Tim Martin, CPA and delivered in 2 hours.

Need it today? Submit before 12PM EST for same-day rush delivery — 2 hours.