Ignition Tax prepares Fannie Mae and Freddie Mac compliant CPA business funds letters — confirming the fund withdrawal will not harm your business’s liquidity, operations, or ability to pay debts. $199. Delivered in 2 hours.

Fannie Mae Selling Guide (B3-4.2-01) and Freddie Mac Single-Family guidelines both address the use of business assets for down payments by self-employed borrowers. Both require documentation confirming the business can sustain operations after the withdrawal. For most lenders following these guidelines, a CPA letter is the required form of this documentation — because only a licensed CPA, as an independent third party who has reviewed the business’s financial records, can provide the required verification.

The CPA letter specifically confirms: the borrower’s percentage of business ownership and legal authority to withdraw funds, that the business funds being used have already been subject to applicable taxes (for S-Corps, sole proprietors, and pass-through entities), that the withdrawal will not impair the business’s solvency or short-term cash flow, and that the business has been continuously operating and generating income for the specified period.

Every Ignition Tax CPA letter for use of business funds is personally prepared and signed by Tim Martin, CPA — licensed in New York State, AICPA member — based on a thorough review of your business financial records, written to align with your specific lender’s requirements and Fannie Mae or Freddie Mac guidelines, and delivered directly to your underwriter in 2 hours.

Underwriters need confirmation that the cash drain will not prevent the company from meeting its short-term operating costs, payroll, or vendor debts after the withdrawal. The CPA — as an independent professional who has reviewed the business's financial records — is the only party who can credibly confirm the business has sufficient remaining cash flow to sustain operations.

Lenders must verify that the borrower has the legal authority to withdraw the funds — specifically 100% ownership or majority shareholder voting rights. This prevents situations where a borrower withdraws business funds without the legal standing to do so, which would violate partnership agreements or operating agreements.

For lending purposes, business funds and personal funds must be treated as separate assets. The CPA letter adheres to proper accounting practices and addresses any concerns about entity separation — confirming the withdrawal is a legitimate, documentable business-to-personal fund transfer that clears any concerns about commingling or improper use.

Tim Martin, CPA reviews your business financial records and prepares a letter addressing all three lender verification points — written to your specific lender’s exact requirements and Fannie Mae / Freddie Mac guidelines.

If a CPA signs a letter guaranteeing the business will remain healthy, and the business later defaults or fails, the mortgage lender can sue the CPA for negligent misrepresentation.

Errors and Omissions (E&O) insurance providers typically exclude coverage for liability stemming from unauthorized third-party comfort letters — leaving the CPA personally exposed to claims.

AICPA explicitly prohibits CPAs from providing assurances about future financial events they cannot verify — including future solvency guarantees or predictions about business performance.

The solution is not avoiding the letter — it is writing it correctly. An AICPA-compliant CPA letter does not guarantee future solvency or predict future performance. Instead, it confirms specific, verifiable historical and current facts:

The borrower is the legal owner of the business — verified from business records and filings

The business has been operating and generating income — verified from reviewed tax returns.

Based on current reviewed financial records, the withdrawal does not appear to impair current operational capacity

The business funds represent already-taxed income — not subject to additional tax on distribution (for S-Corps, sole proprietors)

This factual, historical framing is exactly what Fannie Mae and Freddie Mac require — and it is what protects the CPA from professional liability. Tim Martin, CPA prepares every business funds letter within AICPA professional standards — providing exactly what your lender needs without exposing the CPA to legal or E&O risks.

If your previous CPA declined — or if your lender rejected a previous letter — Ignition Tax prepares the letter correctly at $199. No prior relationship needed. Submit your lender’s requirements and we start the same day.

Not sure if you need the letter or an alternative? Message us — we confirm within minutes at no charge which approach applies to your specific situation.

The CPA's confirmation that the borrower is the legal owner of the business — including ownership percentage and any relevant shareholder or partner authority — confirming the legal standing to withdraw funds from the business account

A statement that the business has been continuously operating and generating income — confirming the business is not newly formed or dormant — and that based on the CPA's review of current financial records, the business is financially active

The primary statement: that based on the CPA's review of current financial records, the withdrawal of the specified amount will not negatively impact the business's liquidity, operations, or ability to meet its financial obligations — written as a factual historical assessment, not a future guarantee

For pass-through entities (S-Corporations, sole proprietors, partnerships), a statement that the funds represent income already reported and taxed on the borrower's personal tax returns — and are therefore not subject to additional tax liability upon distribution

Personally signed by Tim Martin, CPA — NY State license number visible on official letterhead. The active license number allows lenders to independently verify CPA credentials with the state licensing board before accepting the letter

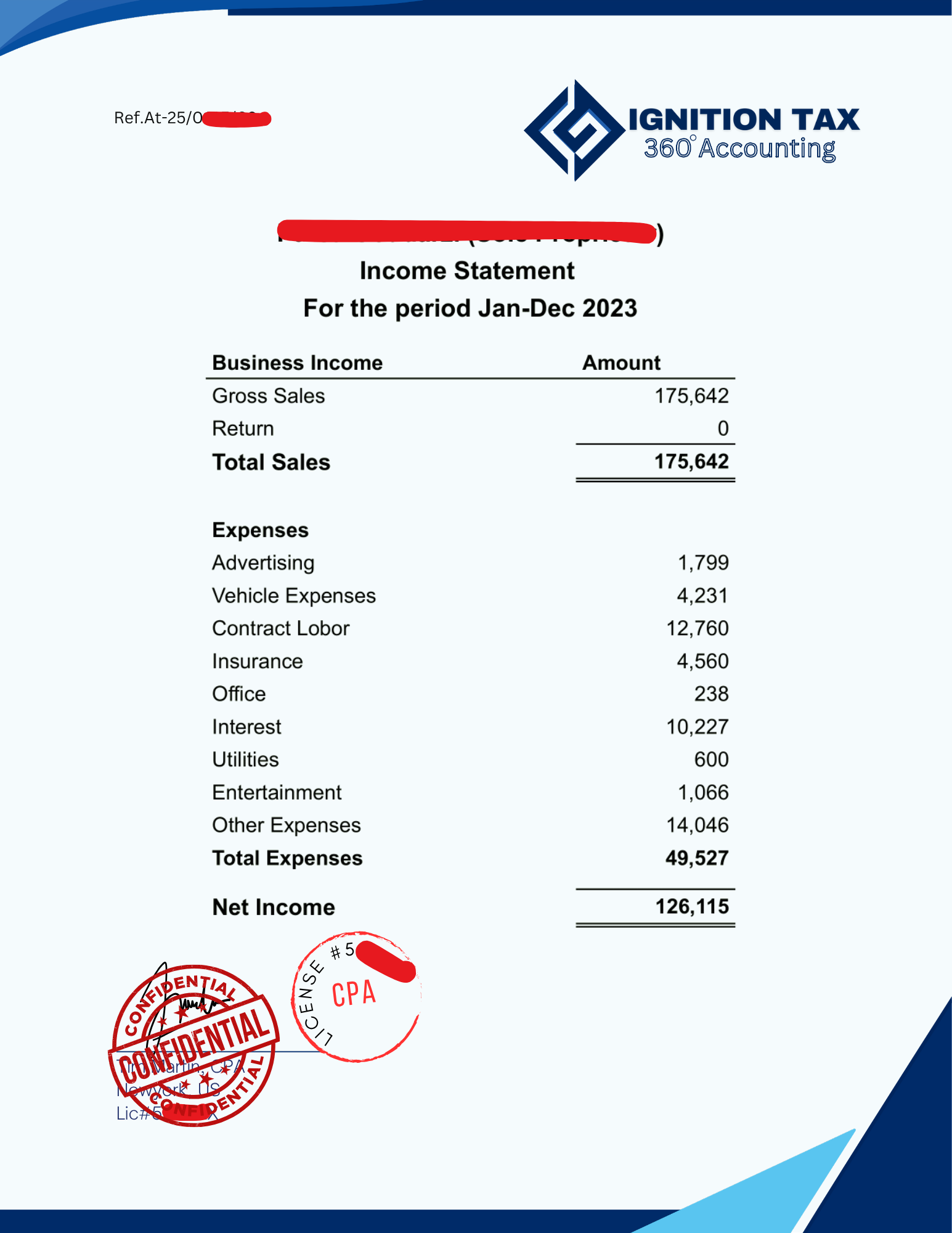

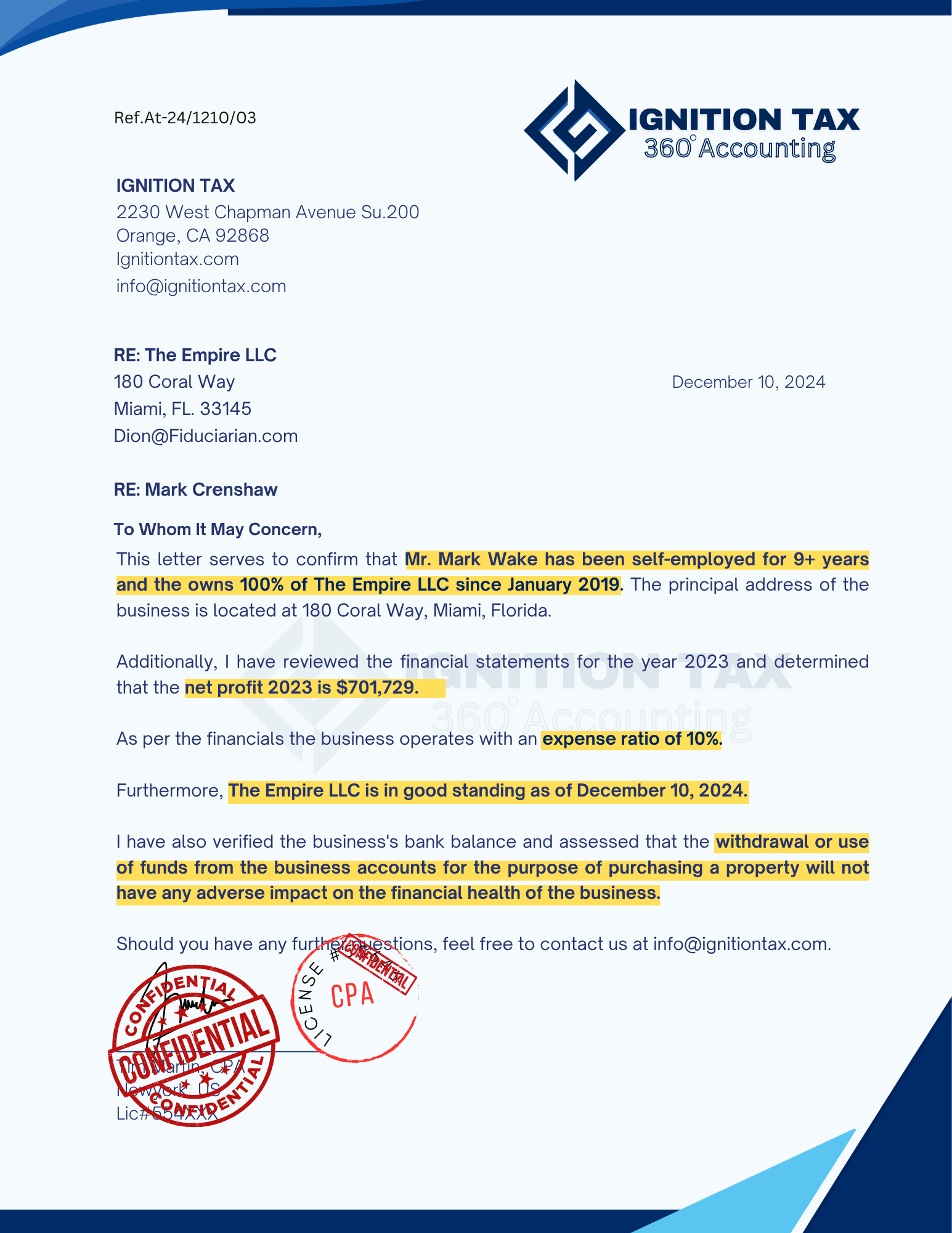

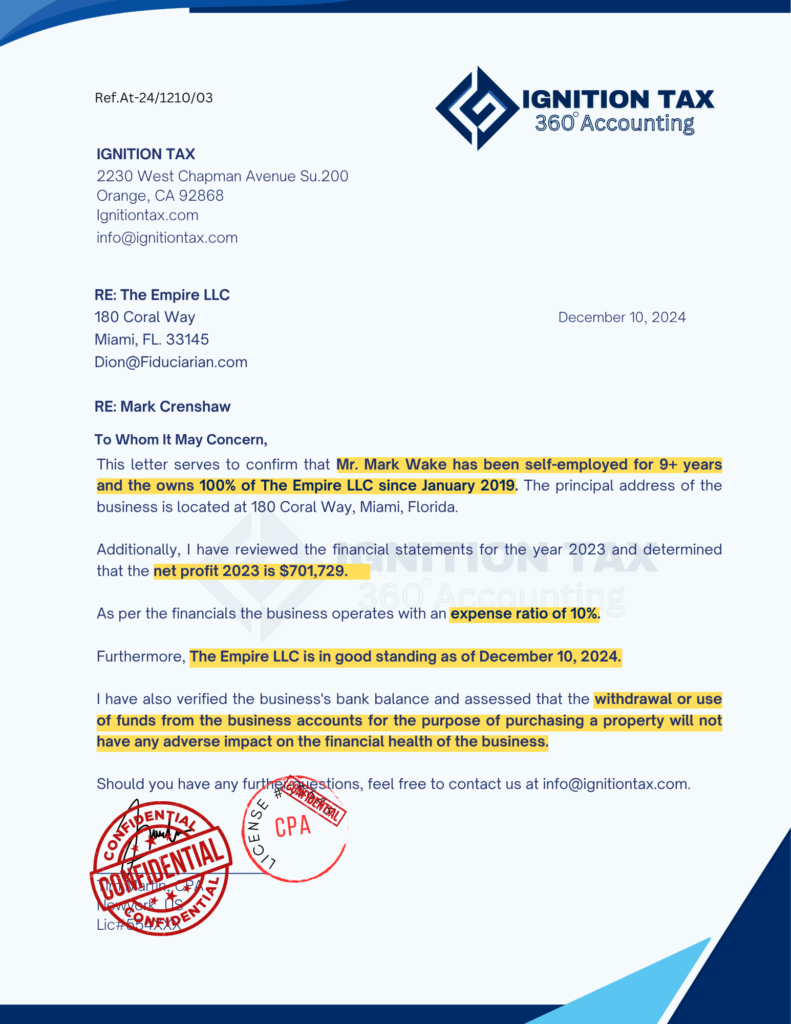

Sample Ignition Tax CPA letter — format follows AICPA professional standards

The most common scenario. You are self-employed, your savings are in a business account, and you need to move funds to close on a home. Your lender requires documentation confirming you own the business, have authority to withdraw, and that the withdrawal will not impair the business.

Some borrowers have personal funds for the down payment but need business funds to cover closing costs — origination fees, title insurance, prepaid taxes. Fannie Mae guidelines treat closing cost sourcing the same as down payment sourcing — a CPA letter is required in both cases.

For S-Corp shareholders and partnership members, funds held in the business represent taxed income that has already flowed through to personal tax returns. A CPA letter confirms both the legal authority to withdraw and the tax treatment of the distribution — often paired with an expense ratio letter.

When one borrower on a joint mortgage application is self-employed and contributing business funds — even if the primary borrower is W-2 employed — the lender still requires a CPA business funds letter for the self-employed co-borrower's fund contribution.

Not sure if your situation requires this letter? Message us — we confirm within minutes at no charge.

Every letter uses factual historical framing — AICPA compliant. No future solvency guarantee, no language that creates professional liability. This is exactly what Fannie Mae and Freddie Mac require — and what your underwriter will accept.

Order at $199. Provide lender name, exact wording your underwriter requested, amount being withdrawn, and source account. Previous CPA refused? Tell us what language they declined — we'll tell you how to address it.

Upload: federal tax returns (2 years), P&L statement, 2–3 months business bank statements, business entity documents (operating agreement showing ownership), and lender's checklist.

Tim Martin personally reviews all records, confirms ownership authority, assesses withdrawal impact, and determines correct AICPA-compliant wording for your business structure (LLC, S-Corp, sole proprietor, partnership).

We share a draft addressing your underwriter's requirements. We flag any language outside AICPA standards and confirm wording satisfies your lender before finalizing.

Signed letter delivered directly to your mortgage lender or underwriter via secure email — or to you for forwarding. Notarization available for $349.

We are currently in the process of obtaining a mortgage loan, and the lender requires a CPA letter to verify the following details:

Our lenders require a letter that verifies the business expense ratio, which is 15%. Additionally, the letter should state that “the use of business funds does not have any adverse impact on the business”.

We are currently in the process of fulfilling a request for our tenant, who requires a letter to verify the following details for housing purposes:

CPA Letter for Self Employed or Business owners needs a CPA letter for mortgage lender

CPA Letter Plus for Business Partners, Self Employed Individuals need a CPA letter with Notarization

Licensed Certified Public Accountant

Fannie Mae and Freddie Mac guidelines require this letter to be signed by a licensed Certified Public Accountant — not a bookkeeper, enrolled agent, or business owner. Tim Martin holds an active NY State CPA license verifiable with the New York State Board of Regents.

Every business funds letter uses factual, historical wording within AICPA professional standards — no future solvency guarantees, no language that creates professional liability. The letter provides exactly what Fannie Mae and Freddie Mac require without exposing Tim Martin to the legal and E&O risks that cause other CPAs to refuse. This is why our letters get accepted when others are rejected.

Business funds letters supporting successful conventional, FHA, VA, jumbo, and portfolio loan approvals across all self-employed business structures — LLCs, S-Corps, sole proprietors, partnerships — in all 50 US states.

If your underwriter requests wording revisions, we revise at no charge. If we cannot satisfy your lender's requirements within AICPA standards, we provide a full refund — no questions asked.

NY State License

Professional Compliance

Tax Return Verified

All 50 States

Available — $349

Ignition Tax charges $199 for a standard CPA letter for use of business funds, delivered in 2 hours. A notarized version is $349. This is a flat fee covering document review, letter preparation, lender-specific wording, and direct delivery to your underwriter — no hourly billing, no hidden charges. No competitor on this SERP publishes their price — $199 is the only transparent rate available for this specific letter type.

Ignition Tax delivers standard business funds letters in 2 hours when all documents are submitted. Notarized delivery is available in 24 hours — submit before 12PM EST. This is one of the most common rush letter types because mortgage closings often have same-day or next-day documentation deadlines. Ignition Tax has delivered business funds letters in under 2 hours fast delivery.

Still have questions?

Income verification and comfort letters for mortgage underwriters — Fannie Mae and Freddie Mac aligned

Third-party verification letter for mortgage brokers and lenders — all self-employed income types

Self-employment status and income verification — mortgage, rental, visa, and business loan applications

Business expense ratio verification for non-QM bank statement loans — often ordered alongside business funds letter

Income confirmation from tax returns and P&L for all lender types and loan programs

See all 12 types of CPA letters we prepare for self-employed individuals

Licensed, AICPA-compliant CPA letters for use of business funds — prepared by Tim Martin, CPA within Fannie Mae and Freddie Mac guidelines. Delivered in 2 hours. Accepted by all mortgage lenders.

Need it today? Submit before 12PM EST for same-day fast delivery — 2 hours.