We prepare licensed, AICPA-compliant CPA letters accepted by Fannie Mae, Freddie Mac, FHA, and conventional lenders — delivered in 2 hours, directly to your underwriter.

A CPA letter for a mortgage — also called a comfort letter, third-party verification letter, or CPA income verification letter — is a formal document prepared by a licensed Certified Public Accountant that verifies a self-employed borrower’s business existence, income stability, ownership percentage, and financial health to a mortgage lender or underwriter.

Mortgage lenders following Fannie Mae, Freddie Mac, FHA, and VA guidelines require independent income verification from all borrowers. For self-employed individuals, sole proprietors, LLC owners, S-Corp shareholders, and 1099 contractors, a CPA letter provides the third-party verification that satisfies underwriting requirements. Without it, self-employed borrowers face loan denials even when their actual income easily qualifies them.

Sole proprietors, freelancers, and independent contractors have no employer to verify income. A CPA letter provides the third-party verification Fannie Mae and Freddie Mac require in place of W-2 documentation.

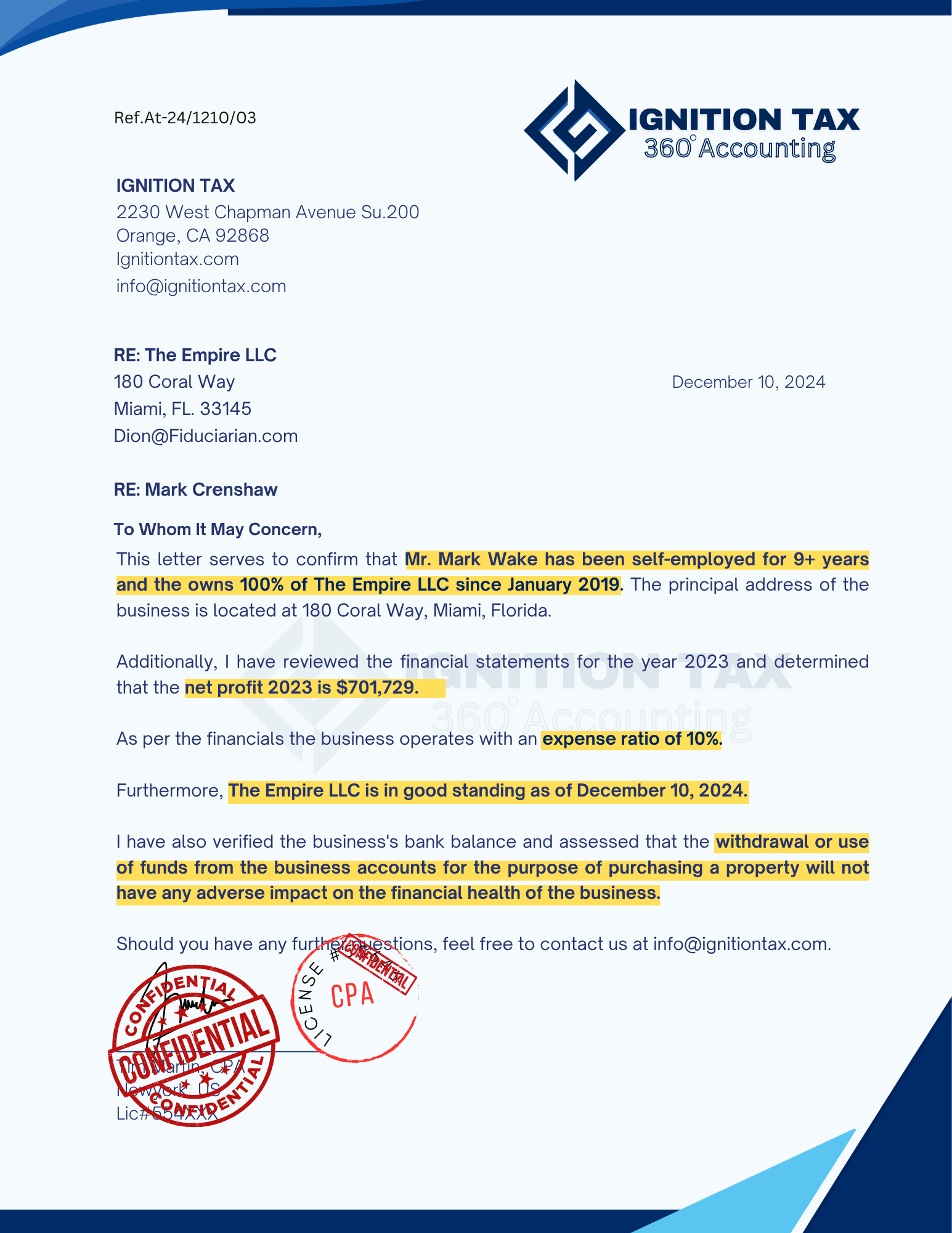

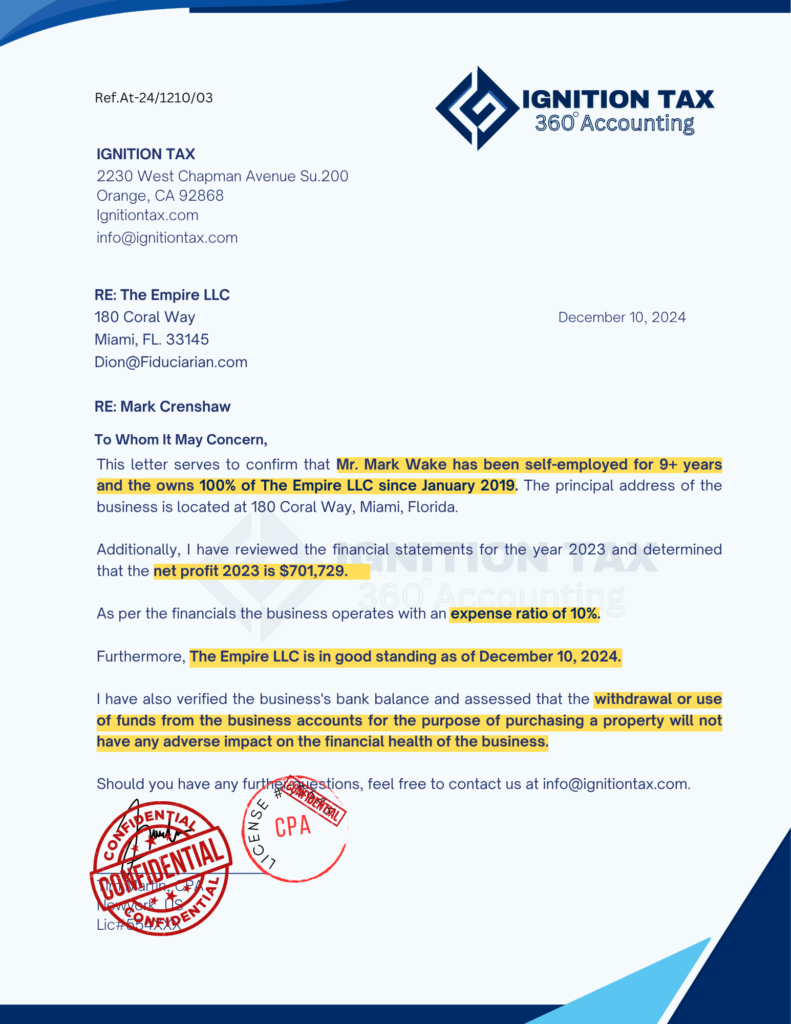

Fannie Mae and Freddie Mac require a specific CPA letter when a borrower withdraws business bank account funds for a mortgage down payment, confirming the withdrawal won't adversely impact business health.

Business owners with complex income structures — K-1 distributions, S-Corp salary plus dividends, or guaranteed payments — need a CPA letter to clarify total qualifying income to underwriters.

When a borrower's most recent tax return shows a significant increase or decrease in income, lenders may request a CPA letter explaining the change and confirming current income from available financial records.

For loan amounts above conventional limits or non-qualified mortgage products, lenders often require additional third-party verification beyond tax returns — a CPA letter satisfies this requirement.

Whatever your business structure, Ignition Tax prepares your CPA letter to exactly match your lender’s requirements and loan type — delivered in 2 hours at $199 flat fee.

Ignition Tax mortgage CPA letters are written specifically to meet Fannie Mae and Freddie Mac underwriting requirements — reducing revision requests and avoiding closing delays. $199 flat fee, delivered in 2 hours.

CPA firm name, address, active state license number, and contact information — confirming the letter comes from a licensed CPA whose credentials lenders can verify with the state board

Preparation date and a unique reference number allowing lenders and underwriters to track the letter throughout the underwriting and closing process

Your specific lender's name, address, and loan reference number — addressed directly to your mortgage lender or underwriter, not a generic form letter

Confirms the borrower has authorized the CPA to release financial information to the named lender — required under AICPA confidentiality standards

Self-employment status, business ownership %, income from reviewed records, expense ratio, business good standing — all verified from actual financial documents

States the letter is based on limited procedures — not an audit, review, or guarantee. Required under AICPA professional standards; protects both the CPA and the lender

Personally signed and stamped by Tim Martin, CPA — NY State license number on every letter. Not outsourced, not AI-generated, not delegated to staff

We provide a complete document checklist immediately after you place your order.

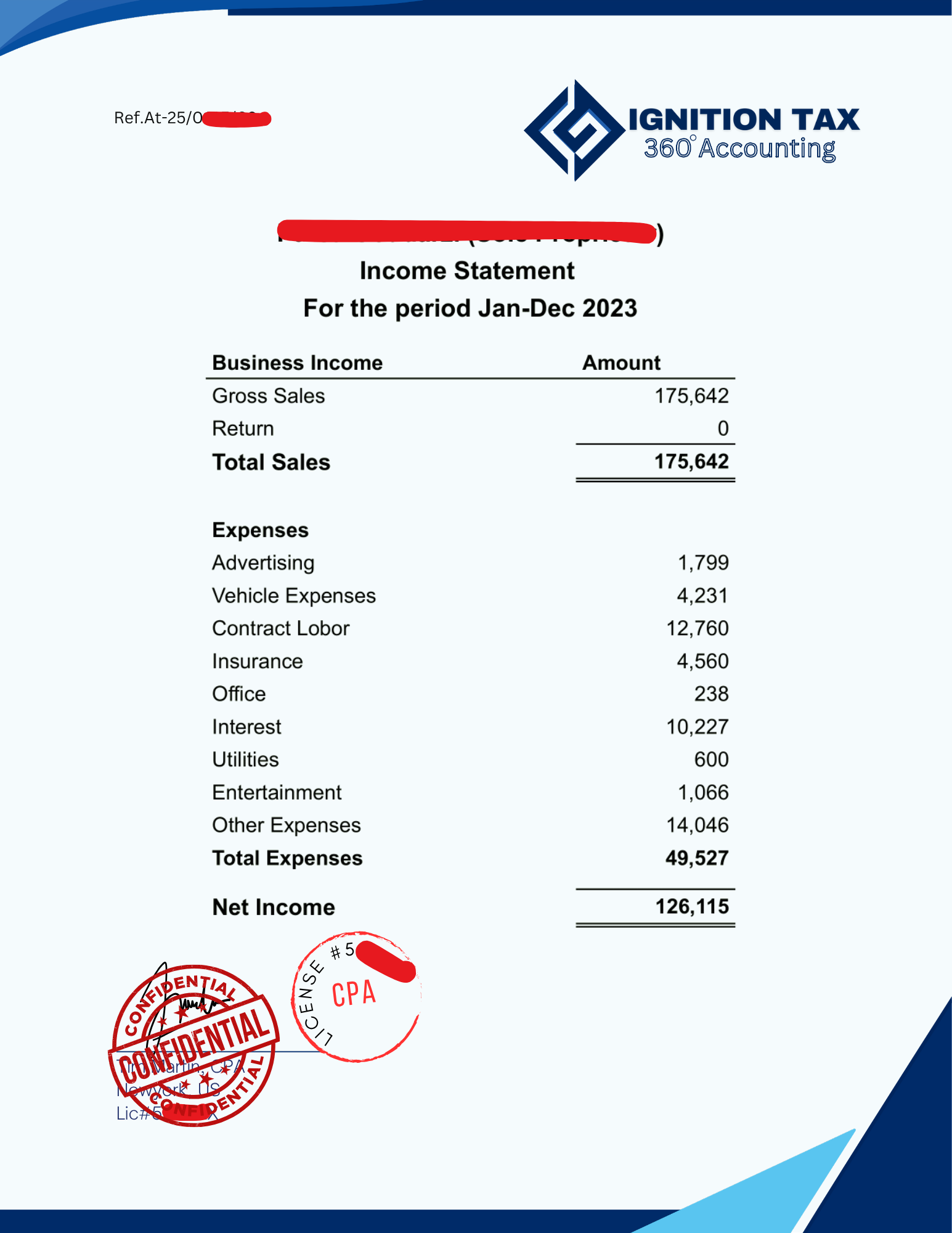

Schedule C filers show after-deduction income that is often much lower than actual revenue. A CPA letter verifies true qualifying income from the CPA's complete financial records review.

LLC owners need a CPA letter to verify ownership percentage, actual income, and — when using business funds for a down payment — that the withdrawal will not harm the business. Both Fannie Mae and Freddie Mac require this.

S-Corp owners receive both W-2 salary and K-1 distributions. Underwriters require a CPA letter to document total qualifying income combining both sources and confirm business sustainability.

Independent contractors with income from multiple clients need a CPA letter to aggregate total qualifying income — often a combination of sources that standard underwriting cannot easily calculate.

Investors and business owners using business bank account funds for a mortgage down payment require a specific CPA letter confirming the withdrawal will not negatively affect business operations — a direct Fannie Mae and Freddie Mac requirement.

Whatever your business structure, Ignition Tax prepares your CPA letter to exactly match your lender’s requirements and loan type — delivered in 2 hours at $199 flat fee.

Bank statement mortgage programs qualify self-employed borrowers using 12–24 months of business bank deposits — without requiring tax returns or a CPA letter. Best when bank statement income significantly exceeds tax return income.

Some lenders — particularly for conforming loans — may accept copies of tax returns alongside a letter stating the CPA prepared the returns, without requiring full third-party income verification. Less common for conventional loans following Fannie Mae guidelines.

A VOSE letter confirms only that a business exists and the borrower is self-employed — without income verification. Some lenders accept this as a supplement to tax returns rather than requiring a full comfort letter.

Not sure which option applies to your specific lender? Message us and we confirm within minutes at no charge.

Still unsure? Message us and we will tell you within minutes — at no charge. We only take your order if you actually need the letter.

If your filed tax returns — at face value — show enough income to qualify for the loan amount you need, many lenders will not request a CPA letter.

Non-QM bank statement loans specifically designed for self-employed borrowers often do not require CPA letters — they qualify income from business bank deposits instead.

If your self-employment is recent and you have prior W-2 income that clearly qualifies you for the loan, some lenders will not require additional CPA documentation.

If your mortgage lender or underwriter has not asked for a CPA letter, you may not need one for your specific loan file.

Borrowers with significant home equity and low loan-to-value ratios sometimes have more flexible documentation requirements from lenders.

Your lender reviews initial documentation. If you are self-employed, they will typically flag that a CPA letter will be required before final approval. Order your letter now — before underwriting begins.

Your lender or underwriter provides a specific list of what the CPA letter must confirm: income, self-employment duration, ownership, expense ratio, and/or business funds use. Share this list with Ignition Tax at order time.

Place your order at $199. Submit tax returns, P&L, and lender checklist. Tim Martin, CPA reviews and prepares your letter to your lender's exact specifications. Delivered in 2 hours.

Your signed CPA letter is delivered directly to your mortgage lender or underwriter via secure email — or to you for forwarding. Addressed directly to your specific underwriter.

Your underwriter reviews the CPA letter alongside your full loan file. If any revisions are requested, Ignition Tax revises at no additional charge under our 100% acceptance guarantee.

With complete documentation including your CPA letter, your loan file proceeds to approval and closing. Most lenders accept CPA letters dated within 60–120 days of closing.

Need your CPA letter for an upcoming closing? Order now for 2 hour delivery →

Fully remote. No office visit. No prior relationship required

Select letter standard at $199 or notarized at $349. Provide your lender's name and specific requirements. Processing begins immediately.

Upload tax returns (1–2 years), P&L statement, and lender checklist. We send a tailored checklist after your order.

Tim Martin personally reviews all documents, verifies facts, and writes a letter to your lender's exact requirements and AICPA standards.

We prepare your letter, share a draft for review, make adjustments, then sign and stamp on official CPA letterhead.

Signed letter delivered directly to your underwriter via secure email. Notarization available for $349 if required.

We are currently in the process of obtaining a mortgage loan, and the lender requires a CPA letter to verify the following details:

Our lenders require a letter that verifies the business expense ratio, which is 15%. Additionally, the letter should state that “the use of business funds does not have any adverse impact on the business”.

We are currently in the process of fulfilling a request for our tenant, who requires a letter to verify the following details for housing purposes:

Flat fee pricing. You see the full cost before we start.

CPA Letter for Self Employed or Business owners needs a CPA letter for mortgage lender

CPA Letter Plus for Business Partners, Self Employed Individuals need a CPA letter with Notarization

Licensed Certified Public Accountant

Tim Martin holds an active CPA license visible on every letter. Lenders and underwriters can verify it directly with the New York State Board of Regents.

Every mortgage letter follows AICPA professional standards and is aligned to Fannie Mae and Freddie Mac underwriting requirements — reducing revision requests and avoiding closing delays.

CPA letters supporting successful mortgage applications — conventional, FHA, VA, jumbo, and non-QM — across all loan types and all 50 US states.

If your lender or underwriter requests revisions, we revise at no charge. If we cannot satisfy your lender's requirements with complete documentation, we provide a full refund — no questions asked.

NY State License

Professional Compliance

Tax Return Verified

All 50 States

Available — $349

Available — $349

Ignition Tax charges $199 for a standard mortgage CPA letter (2 hours) and $349 for notarized or complex letters involving multiple tax years, S-Corp structures, or multi-entity income (24 hours). Ignition Tax flat fee covers all document review, letter drafting, lender-specific wording, and direct delivery to your underwriter.

Order online at ignitiontax.com and provide your lender’s name and specific requirements. Submit your tax returns (1–2 years), P&L statement, and lender checklist. Tim Martin, CPA personally reviews your documents and prepares the letter to your lender’s exact specifications. Standard delivery is 2 hours. Notarized letter delivery (24 hours) is available for same-day closing deadlines — submit before 12PM EST.

Ignition Tax delivers standard CPA mortgage letters in 2 hours when all documents are submitted. Notarized letter delivery is available in 24 hours for urgent mortgage closings or same-day underwriting deadlines — submit your order and all documents before 12PM EST. Most underwriters accept same-day CPA letters as long as the letter is dated at least one business day before closing.

Ignition Tax charges $199 for a standard mortgage CPA letter and $349 for notarized or complex letters (multiple tax years, S-Corp structures, multi-entity income). The flat fee includes document review, letter drafting, lender-specific wording, and direct delivery to your underwriter. Fast delivery (2 hours) is available when documents are submitted before 12PM EST. Notarization (for visa or legal use) is $349. There are no hidden fees or hourly billing charges.

Still have questions?

Beyond mortgage letters, Ignition Tax prepares all types of CPA letters for self-employed individuals and business owners

Third-party verification — also called comfort letter — for mortgage brokers and lenders

Confirms income from tax returns and P&L for lenders and landlords

Verifies business fund withdrawal for down payment won't harm business health

Business expense ratio confirmation for mortgage underwriters

Self-employment status and income verification for any loan type

See all 12 types of CPA letters we prepare nationwide

Licensed, AICPA-compliant CPA letters for self-employed mortgage borrowers — prepared by Tim Martin, CPA, accepted by Fannie Mae, Freddie Mac, FHA, and conventional lenders nationwide. Delivered in 2 hours.

Need it today? Submit before 12PM EST for same-day fast delivery — 2 hours.