A CPA letter does not estimate future earnings or guarantee financial performance. It confirms only what the CPA has directly observed, prepared, or reviewed in official financial records — governed by AICPA professional ethics standards.

Self-employed individuals, 1099 contractors, business owners, real estate investors, visa applicants, and individuals in legal proceedings are the primary groups who need CPA letters. At Ignition Tax, every letter is prepared by Tim Martin, CPA — NY State licensed, AICPA member — at $199, delivered in 2 hours.

Tim Martin, CPA · NY State Licensed · AICPA Member

A CPA letter is an official document prepared and signed by a licensed Certified Public Accountant that verifies specific financial facts about an individual or business based on previously reviewed tax returns, financial records, and accounting data.

Lenders, landlords, government agencies, and immigration authorities request a CPA letter when standard income documents — such as W-2 forms or pay stubs — are unavailable or insufficient to confirm financial stability. The letter serves as an independent, third-party verification of income, business ownership, tax compliance, and employment status.

A CPA letter does not estimate future earnings or guarantee financial performance. It confirms only what the CPA has directly observed, prepared, or reviewed in official financial records. According to the American Institute of Certified Public Accountants (AICPA), CPAs are bound by professional ethics standards that limit the content of any verification letter to verifiable, documented facts — and this professional obligation is what gives a CPA letter its credibility as a trusted third-party document.

Self-employed individuals, 1099 contractors, business owners, and freelancers are the 4 primary groups who rely on CPA letters, as these individuals lack the standardized payroll documentation that salaried employees provide automatically through their employer.

Only a licensed Certified Public Accountant with an active state license. Tax preparers, enrolled agents, and bookkeepers without a CPA license cannot prepare a letter that carries the same professional authority. At Ignition Tax, every letter is signed by Tim Martin, CPA — NY State licensed, AICPA member.

A CPA letter is referred to by 6 common alternative names depending on the context in which it is requested. All 6 names refer to the same category of document — a professionally prepared, CPA-signed statement verifying financial information.

The most widely used alternative name. Mortgage lenders and mortgage brokers commonly use "comfort letter" when requesting third-party income verification from a CPA. The term reflects the document's purpose — providing comfort to the requesting party that the financial information presented is accurate and professionally verified.

Used in formal lending and underwriting contexts. This name emphasizes that the verification comes from an independent professional who is not the borrower, the lender, or the employer — making it the most technically precise name under AICPA professional standards.

A general term used by landlords, property managers, and rental agencies. It refers to any professionally prepared letter confirming income or financial stability, though it carries less legal weight than a letter specifically signed by a licensed CPA with an active state license number.

Used interchangeably with "CPA letter" in mortgage underwriting. This version emphasizes the verification function of the document rather than the comfort it provides. Fannie Mae and Freddie Mac underwriters commonly use this term in their guidelines for self-employed borrower documentation.

Used specifically when the primary purpose is to confirm gross or net income figures for self-employed individuals. The most frequently requested type by mortgage lenders and landlords. Directly replaces the W-2 form as the income verification document for self-employed applicants.

Occasionally used in immigration and legal contexts to describe a CPA letter that certifies specific financial facts about an individual or business for an official proceeding. USCIS adjudicators and consular officers most frequently use this term when requesting financial supporting documents for visa petitions.

A tax return is a legal filing submitted to the IRS reporting income and tax liability for a specific year. A CPA letter references tax return information but serves a different function — it translates that information into a verified statement for a third party. Lenders frequently require both documents together: the tax return provides the raw data and the CPA letter provides the professional interpretation.

An audited financial statement is a comprehensive examination of a company's complete financial records conducted under Generally Accepted Auditing Standards (GAAS). An audit takes weeks or months and costs $5,000–$50,000+. A CPA letter is a significantly shorter document confirming specific facts without conducting a full audit. For most mortgage, rental, and visa applications, a CPA letter is sufficient and far more practical.

A profit and loss (P&L) statement summarizes revenues, costs, and expenses over a specific period. While a CPA letter may reference P&L figures, it is not the same document. Some lenders request both — the P&L as the underlying financial record and the CPA letter as the professional verification of that record's accuracy.

A CPA letter confirms historical financial facts. It does not predict future income, guarantee loan repayment ability, or certify future business performance. Under AICPA professional standards, a CPA who includes forward-looking guarantees in a verification letter violates professional ethics rules and assumes significant legal liability. Receiving a CPA letter does not guarantee mortgage, visa, or rental approval — it provides the verified financial documentation the requesting party uses to make their own decision.

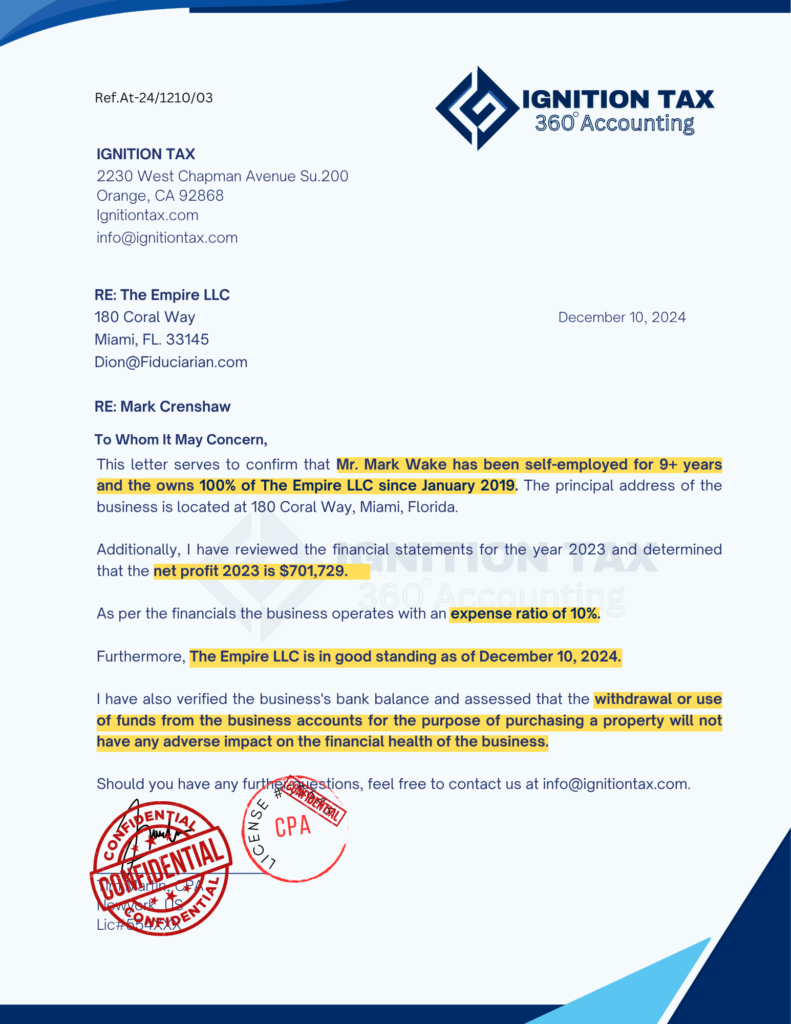

The most frequently requested CPA letter type. A written statement signed by a licensed CPA confirming a specific individual's gross or net income based on filed tax returns and reviewed financial records. Requested by mortgage lenders, landlords, and government agencies when an applicant cannot provide standard W-2 income documentation. Fannie Mae and Freddie Mac both require a CPA income verification letter for self-employed borrowers who cannot document income through W-2s. Must confirm the business is actively operating and that income figures align with filed tax returns.

A written statement signed by a licensed CPA that confirms an individual's or entity's total net worth based on reviewed financial records, asset documentation, and liability information. Rather than confirming ongoing income, it confirms total financial position at a specific point in time. Requested in 3 primary contexts: (1) Accredited investor verification — SEC requires $1 million net worth excluding primary residence, (2) Immigration petitions — E-2 and EB-5 investor visas require documented proof of investable net worth, (3) Business partnership agreements — partners entering high-value agreements request net worth verification.

The broadest of the 6 CPA letter types — functions as a comprehensive verification document addressing multiple financial attributes in a single letter. Mortgage lenders are the most frequent requesters. The defining characteristic is the statement that the CPA has no knowledge of any material changes to the business that would affect income stability. Must meet Fannie Mae, Freddie Mac, FHA, and conventional lender requirements for self-employed mortgage applicants. Contains 6 standard elements: CPA credentials, client is active tax client, business is actively operating, income figures from 2 most recent tax years, business ownership percentage, and the material change statement.

A formal professional document in which a licensed CPA provides an expert opinion on a specific financial, accounting, or tax matter based on reviewed records, applicable law, and professional judgment. Differs from the other types in one critical way — it expresses professional judgment rather than factual verification alone. Used in 4 primary contexts: (1) Tax position opinions — confirming a tax strategy is legally supportable under the IRC, (2) Business valuation opinions — estimated fair market value for business sales or divorce proceedings, (3) Financial compliance opinions — confirming practices comply with applicable standards, (4) Litigation support opinions — expert financial evidence in courts. Carries the highest professional liability of all letter types.

A formal communication issued by a CPA to the leadership of a business that identifies internal control weaknesses, accounting deficiencies, and financial reporting issues discovered during an audit or review engagement. This type is fundamentally different from the other 5 — it is not a third-party verification document for lenders or landlords. It is an internal professional communication directed at business owners or executives. Serves 3 primary functions: (1) Reporting internal control deficiencies discovered during audit, (2) Recommending corrective actions, (3) Creating an accountability record. Required under AICPA auditing standards when significant deficiencies or material weaknesses are discovered. Used by businesses seeking external financing, preparing for acquisition, or responding to regulatory review.

A standard CPA letter additionally authenticated by a licensed notary public who verifies the identity of the CPA signatory and witnesses the signing of the document. Notarization adds a layer of legal authentication — confirming the signer's identity, that they signed voluntarily, and creating a verifiable official record with date and time. Required in 4 specific situations: (1) International visa applications through foreign consulates, (2) Certain USCIS immigration petitions specifying notarized supporting documentation, (3) Legal proceedings in jurisdictions requiring notarized financial evidence, (4) International business transactions with parties operating under civil law systems — particularly in continental Europe and Latin America.

The CPA's full legal name, active license number, state of licensure, firm name, address, phone, and email. The requesting party uses this to verify the CPA's license status through the state board of accountancy. A letter without firm letterhead raises immediate authenticity concerns with underwriters.

Most lenders impose a validity window of 60–120 days from the date of issuance. Fannie Mae requires the letter to be dated within a specific period relative to the loan application date. A letter issued outside the acceptable window is rejected regardless of its content.

A professionally prepared CPA letter identifies the specific party to whom it is addressed — the lender, landlord, agency, or institution requesting verification. Generic letters addressed "To Whom It May Concern" are rejected by large mortgage lenders and government agencies that require institution-specific documentation.

Identifies the client by full legal name and confirms how long the CPA has prepared the client's taxes or managed their financial records. A statement such as "I have prepared the federal and state income tax returns for [Client] for the past [X] years" establishes documented familiarity with the client's financial history.

The core of most CPA letters. States the client's gross annual income and net income figures derived directly from filed tax returns for the 2 most recent tax years. For self-employed individuals, income is drawn from Schedule C (sole proprietors), Schedule K-1 (partnerships and S-Corp shareholders), or Form 1120S (S-Corporation returns).

Confirms 4 business facts: the legal name of the business, the entity type (sole proprietorship, LLC, S-Corporation, partnership), the client's ownership percentage, and the date the business was established. Fannie Mae's Selling Guide requires lenders to verify that the business is actively operating at the time of the loan application.

Confirms the client is current on all federal and state tax filings. Addresses a specific concern — that the applicant has no outstanding tax liabilities that could affect financial stability or result in IRS liens against their assets or income. For SBA loan applications, tax compliance confirmation is a mandatory component.

The letter closes with the CPA's formal attestation that all information is based on reviewed financial records and prepared in accordance with applicable professional standards. Includes the required AICPA scope disclaimer — stating the letter does not constitute an audit, review, or compilation of financial statements under GAAS.

The largest group requiring CPA letters. Self-employed individuals — sole proprietors, independent contractors, and partnership members — report income on Schedule C of their federal tax return rather than receiving a W-2. Lenders, landlords, and government agencies cannot verify this income through employer payroll systems. Self-employed individuals need a CPA letter in 5 common situations: applying for a conventional, FHA, VA, or jumbo mortgage; renting an apartment or commercial property; applying for an SBA loan or commercial line of credit; sponsoring a family member's immigration petition; and verifying income for court-ordered child support or alimony calculations. Fannie Mae Selling Guide B3-3.2-01 specifically identifies the CPA letter as an acceptable form of third-party verification for borrowers who cannot document income through W-2s.

1099 contractors receive IRS Form 1099-NEC from clients rather than W-2s from employers. They work for multiple clients, earn variable income across different payment sources, and lack the consistent monthly paycheck that lenders use as the baseline for income verification. A CPA letter for a 1099 contractor confirms 3 critical facts: the total annual income earned across all 1099 sources as reported on filed tax returns, the consistency of income over the 2 most recent tax years, and the active status of the contractor's freelance or consulting practice. Gig economy workers — rideshare drivers, delivery contractors, platform-based freelancers — fall into this category.

Business owners who draw income from their company face a unique verification challenge. An S-Corporation shareholder receives both a W-2 salary and a K-1 distribution from business profits. Lenders calculating qualifying income must account for both streams — requiring professional verification beyond what a standard W-2 provides. Business owners need CPA letters in 4 specific situations: mortgage applications (including business funds verification under Fannie Mae B3-4.2-01), Non-QM loan applications requiring an expense ratio letter, SBA loan applications, and partnership and investor agreements requiring independent financial verification.

Real estate investors who own rental properties face a specific documentation challenge. Rental income reported on Schedule E is frequently offset by depreciation deductions, mortgage interest, and property expenses — producing a taxable income figure that appears lower than the investor's actual cash flow. A CPA letter for a real estate investor confirms 3 facts lenders need beyond what tax returns show directly: the actual rental income generated before non-cash deductions, the add-back calculations for depreciation and other allowable deductions, and the active operating status of the rental portfolio. Used for portfolio loans, DSCR loans, and conventional investment property mortgages.

USCIS and foreign consulates request CPA letters for 5 visa and immigration categories: Employment-Based Visas (O-1, EB-1, EB-2) for self-employed petitioners; Investor Visa Applications (E-2, EB-5) requiring documented proof of investable assets and net worth; Form I-864 Affidavit of Support for family-based green cards — self-employed sponsors must demonstrate income at 125% of the federal poverty guideline; and B-1/B-2 Tourist and Business Visitor Visas where consulates request proof of financial ties and self-sufficiency.

Courts, attorneys, and financial institutions request CPA letters as independent financial evidence in 4 legal contexts: (1) Divorce and family law proceedings — family courts rely on CPA letters to verify income of self-employed spouses when calculating child support and spousal support, (2) Business disputes and partnership dissolutions — provides independent financial verification of income history and asset values, (3) Child support and alimony modification proceedings — confirmed current-year income from the most recently filed return, (4) Bankruptcy proceedings — trustees require professionally verified documentation of income and assets. In all legal contexts, a CPA letter carries greater evidentiary weight than self-reported financial statements because it represents the professional judgment of a licensed, credentialed third party who assumes legal responsibility for the accuracy of the information.

A CPA letter serves 6 primary use cases across lending, real estate, immigration, and legal contexts. Understanding each use case prepares applicants to request the correct letter type and meet specific requirements on the first submission.

Confirms a self-employed borrower's income, business operating status, and financial stability for conventional, FHA, VA, or jumbo loan underwriting. Fannie Mae Selling Guide B3-3.2-01 identifies 4 specific requirements: current business operating status, income from 2 most recent tax years, business ownership percentage, and CPA license and contact information. Freddie Mac requires the letter to be dated within 120 days of the note date for purchase transactions.

The SBA requires independent financial verification for 3 primary loan programs: SBA 7(a) loans (up to $5 million), SBA 504 loans (major assets and commercial real estate), and SBA Microloan Program (up to $50,000). Commercial lenders outside the SBA program also require CPA letters to verify 4 facts: sufficient income to support loan repayment, active business operating history, stated ownership percentage, and no outstanding federal tax delinquencies.

Landlords and property managers request CPA letters to satisfy standard income-to-rent ratio requirements (typically 2.5–3x monthly rent). A CPA letter for a rental application addresses 3 specific landlord requirements: income-to-rent ratio verification from filed tax returns, income consistency over the 2 most recent tax years, and confirmation that the business generating the income is currently active.

Used in 5 immigration contexts: Form I-864 Affidavit of Support (self-employed sponsors at 125% poverty guideline), E-2 Treaty Investor Visa (substantial personal investment in a U.S. business), EB-5 Immigrant Investor Visa (minimum $800,000–$1,050,000 investment), O-1 and EB-1 Extraordinary Ability Petitions (income consistent with extraordinary ability), and B-1/B-2 Visitor Visa Applications (financial sufficiency and home country ties).

Fannie Mae Selling Guide B3-4.2-01 requires a CPA letter confirming that a business fund withdrawal for a mortgage down payment does not negatively impact the business. Applies in 3 specific situations: business checking or savings account funds, business investment account liquidation, and S-Corporation or partnership distributions. The CPA's confirmation is based on reviewed bank statements, current P&L figures, and historical cash flow patterns.

Courts and legal counsel request CPA letters in 4 contexts: (1) Divorce and family law — verifying self-employed spouse income for child support and spousal support calculations (American Academy of Matrimonial Lawyers identifies this as one of the 3 most contested financial issues in divorce proceedings), (2) Business disputes and partnership dissolutions, (3) Child support and alimony modification proceedings, (4) Bankruptcy proceedings — trustees require professionally verified income documentation.

Fannie Mae, Freddie Mac, and FHA require both documents together — not as alternatives. A tax return alone is insufficient because it does not confirm current business operating status — a requirement Fannie Mae B3-3.2-01 imposes explicitly. The CPA letter fills this gap by addressing the current operating status of the business at the time of the application.

Bank statements show the movement of money through an account but do not identify the source, nature, or tax treatment of the funds deposited. For self-employed individuals, bank statements show total deposits — which may include business revenue, personal transfers, loan proceeds, asset sales, and other non-income items. A lender cannot distinguish between taxable income deposits and non-income deposits without additional professional analysis.

A CPA letter provides 4 specific advantages over bank statements alone:

Identifies specific income figures relevant to the lender's qualification calculation. Bank statements show all deposits without distinguishing income from non-income items.

Confirms income figures align with filed tax returns — a discrepancy that bank statements frequently show and cannot themselves explain.

Confirms the business generating the income is currently active. Bank statements confirm only that deposits occurred — not current business status.

Signed by a licensed professional who assumes legal responsibility for its contents. A bank statement is a system-generated record with no professional verification layer.

A P&L statement can be prepared by the business owner, their bookkeeper, or their accountant. It does not carry an inherent verification standard — a self-prepared P&L carries no professional accountability. A CPA letter adds 3 layers of value: professional verification of P&L accuracy, tax return reconciliation, and current business status confirmation. FHA under HUD Handbook 4000.1 requires a CPA-prepared or CPA-reviewed year-to-date P&L statement — effectively combining the P&L and CPA letter into one professional document.

An audited financial statement represents the highest level of financial verification — requiring 4–12 weeks and costing $5,000–$50,000+. A CPA letter provides targeted verification of specific facts at a fraction of the cost and time. An audit is required for: large commercial real estate financing above $5 million, institutional investment and private equity due diligence, and SBA loans above $2 million. For the vast majority of mortgage, rental, immigration, and legal proceedings, a CPA letter is the appropriate and practical choice.

AICPA Statements on Standards for Attestation Engagements (SSAE) and the AICPA Code of Professional Conduct establish 5 firm boundaries on what a CPA letter cannot contain. These boundaries exist to protect 3 parties — the CPA from professional liability, the requesting institution from unverifiable information, and the public from fraudulent financial verification.

A CPA letter contains only historically verified income figures. Any language implying a forward-looking income guarantee falls outside the professional boundaries of a CPA verification letter. This is the most frequently misunderstood aspect of CPA letters among applicants and lenders.

A CPA letter does not state that a client has the ability or intention to repay a loan. Loan repayment ability involves factors beyond the CPA's professional knowledge — future income stability, expense commitments, and financial behavior. The underwriting decision belongs to the lender, not the CPA.

A CPA can only include information they have directly reviewed, prepared, or verified. Income from a tax return prepared by a different preparer, asset values assessed by a different professional, or verbal information without supporting documentation cannot be included.

A licensed CPA cannot prepare a verification letter for an individual or business whose financial records they have not reviewed. This is why some applicants approaching a new CPA are told a records review engagement must be completed first.

Statements such as "I recommend this client for approval" or "this individual is financially responsible" fall outside professional financial verification and are excluded by CPAs who follow AICPA professional conduct standards.

The solution is not avoiding the letter — it is writing it correctly within AICPA standards. Tim Martin, CPA prepares every letter with factual, historical wording that confirms what can be verified — without the future guarantees that create professional liability.

Confirms income, self-employment duration, business structure from reviewed records — without predicting future performance

Every letter includes the required disclaimer — confirming the letter is based on reviewed records and does not constitute an audit

If your lender's requested wording falls outside AICPA standards, Tim Martin prepares an AICPA-compliant alternative that satisfies the lender's underlying requirement

Ignition Tax reviews every letter against the requesting institution's specific requirements before delivery — reducing lender rejection to near zero

A CPA who includes prohibited content faces 3 categories of professional consequence: (1) AICPA disciplinary action — investigation by the Professional Ethics Division, potential membership termination, (2) State Board of Accountancy sanctions — formal reprimand, license suspension 1–5 years, or permanent revocation, (3) Civil and criminal liability — malpractice claims for losses caused by false statements, and potential federal fraud charges.

Want to see the exact structure with every field explained? Our cpa letter template shows the complete copy-paste format — letterhead, consent statement, verified facts, and scope limitations — and what changes for each letter type.

Before contacting a CPA, identify exactly what the requesting institution — lender, landlord, immigration authority, or court — requires the letter to contain. Fannie Mae specifies the letter must confirm current business operating status and income from the 2 most recent tax years. USCIS specifies the financial figures relevant to the specific petition category. Some landlords provide a required template. Collecting specific requirements before contacting the CPA eliminates revisions and ensures the letter meets the institution's standards on the first submission.

Assemble the financial documents the CPA needs before the first contact. A CPA letter is prepared from reviewed financial records — the CPA cannot write the letter from memory or from verbal information. Core documents for most letters: signed federal tax returns (1–2 years), current year-to-date P&L statement, 2–3 months of business bank statements, and business formation documents. After ordering, Ignition Tax sends a tailored document checklist covering exactly what your specific letter type requires.

Complete Documents Checklist by Letter Type →

Contact a CPA who holds an active state CPA license and has experience preparing verification letters for the specific purpose required. Confirm 3 things before engaging: (1) Have they prepared CPA letters for your specific purpose — mortgage, SBA loan, visa, or legal proceeding? (2) Are they familiar with the specific institutional requirements — Fannie Mae guidelines, USCIS standards, or SBA requirements? (3) Can they deliver within the timeline required? A CPA who cannot answer these confidently lacks the experience required and introduces the risk of a non-compliant letter that delays your application.

Provide the CPA with the name and address of the specific institution the letter is addressed to, the exact format or template the institution requires, and any specific language the institution mandates. Some mortgage lenders provide a required template the CPA must follow precisely. USCIS has specific formatting standards for supporting financial documentation. Providing this information upfront ensures the letter is correctly addressed and formatted for immediate submission without revision requests.

The CPA reviews all provided financial documents, verifies figures against filed tax returns and accounting records, and prepares the letter according to applicable professional standards and the requesting institution's requirements. This review process is what gives the letter its professional credibility — the CPA's signature represents their professional attestation that the figures in the letter are accurate and verifiable. At Ignition Tax, Tim Martin, CPA personally reviews every document submitted and signs every letter.

The CPA issues the completed letter on official firm letterhead with their professional signature, license number, and contact information. Review the letter for accuracy before submitting — confirm all names, income figures, dates, and business details are correct and match the supporting documents submitted alongside the letter. Same-day delivery (submit before 12PM EST) is 2 hours — at $199 price with no rush surcharge.

How Long Does it Take to Get a CPA Letter?

Standard turnaround at Ignition Tax is 2 hours when all required documents are submitted. $199 price — no rush surcharge. Standard CPA letter turnaround time: 2–3 business days industry-wide. Ignition Tax: 2 hours with no additional fee.

Schedule C filers — 5 required documents

Form 1040 with Schedule C — must be signed copies. Shows gross business revenue, total expenses, and net profit for each year.

Current income and expense summary from January 1 to most recent month. Can be prepared in QuickBooks, Wave, or Excel — does not need to be audited.

All pages of statements for all business accounts. Must be complete — partial statements are not accepted.

Confirmation that the business is legally registered and currently active in the state of operation.

Some lenders require the CPA to confirm tax returns provided match IRS transcripts on file.

Business entity owners — 7 required documents

Form 1040 showing all income sources including wages, distributions, and pass-through income.

Form 1120-S (S-Corporation) or Form 1065 (Partnership/Multi-Member LLC) with all schedules attached.

Shows the applicant's share of business income, deductions, and distributions.

Current revenue and expense summary for the business entity.

All pages for all business accounts.

Legal documentation confirming the business entity structure and the applicant's ownership percentage.

Documentation confirming the applicant's ownership stake and role in the business.

Fannie Mae B3-4.2-01 — 4 additional documents

Statements showing the current balance in the business account from which funds will be withdrawn.

Documentation of the transfer from the business account to the personal account used for the down payment.

Confirms the business generates sufficient ongoing revenue to sustain operations after the withdrawal.

Summary of monthly business income and expenses confirming the withdrawal does not create a deficit in operating cash position.

USCIS and consular requirements — 6 core documents

USCIS frequently requires 3 years of tax return history rather than the 2 years standard in mortgage applications.

All income documentation issued to the applicant from employers and clients.

For self-employed applicants and business owners.

Showing current account balances and recent deposit activity.

Brokerage statements, real estate records, retirement accounts — for net worth letter purposes (E-2, EB-5 investor visas).

CPA letter for immigration must reference the applicant's full legal name exactly as it appears on their immigration documents.

Requesting a verification letter from a tax preparer, bookkeeper, enrolled agent, or unlicensed accountant rather than a licensed CPA. Lenders following Fannie Mae and Freddie Mac guidelines, USCIS adjudicators, and SBA underwriters specifically require a letter signed by a licensed CPA — and reject letters from any other financial professional regardless of their experience or the accuracy of the financial information in the letter.

✓ Fix: Verify active CPA license status through NASBA’s CPA Verify database at cpaverify.org before engaging any professional.

Requesting a generic CPA letter without first confirming the specific requirements of the requesting institution. Fannie Mae requires confirmation of current business operating status. USCIS requires financial documentation referencing specific petition categories. SBA lenders require tax compliance confirmation. Some landlords provide a required template. A generic letter satisfies the applicant's own understanding of what is needed — not what the institution actually requires.

Submitting incomplete documentation — missing a year of tax returns, omitting business bank statements, or failing to include business entity formation documents. The CPA cannot complete the letter without requesting the missing items. Each missing document adds a minimum of 1 business day to the turnaround time. For applicants working against a mortgage closing date, rate lock expiration, or visa appointment, this delay has direct financial consequences.

Requesting a CPA letter too early means it may expire before the application is submitted — Fannie Mae requires the letter to be dated within 120 days of the closing date. Requesting too late — contacting a CPA 1–2 days before a mortgage closing without arranging same-day service — creates unnecessary urgency. The optimal timing is 5–10 business days before the application or closing date for standard delivery.

✓ Fix: Request the letter 5–10 business days before the submission date. For hard deadlines within 24 hours, use Ignition Tax’s same-day service — 2 hours, no rush surcharge.

Submitting a CPA letter without the underlying tax returns and financial records. Lenders, landlords, and immigration authorities require the CPA letter and the underlying financial documents as a complete package. Submitting the CPA letter alone raises authenticity concerns — the requesting institution cannot cross-reference the figures in the letter against the underlying documents, creating the suspicion that figures may not align with actual records.

Asking the CPA to include income projections, loan repayment guarantees, or personal character endorsements in the letter. A CPA who agrees to include such content does so at the cost of their professional integrity and license. A CPA who declines — as all properly credentialed professionals do — is sometimes perceived by the applicant as being unhelpful rather than professionally responsible.

Attempting to reuse a CPA letter prepared for a previous application. A letter prepared for a 2023 mortgage application does not satisfy the requirements of a 2025 mortgage application — regardless of whether the financial figures remain accurate. CPA letters are application-specific, addressed to a specific institution, and dated for a specific application. Each new application requires a new CPA letter dated within the institution's required validity window.

Submitting the CPA letter without reviewing it for accuracy. A CPA letter that contains an error in the client's name, income figures, business entity name, or ownership percentage — however minor — creates a discrepancy between the letter and the supporting documents that triggers underwriting questions and delays. Reviewing the letter before submission takes 5 minutes and eliminates the risk of a correction request that delays the application by 2–3 business days.

Inaccurate and fraudulent CPA letters produce 4 categories of serious legal, professional, and financial risk — for the applicant who submits the letter, the CPA who signs it, and the institution that relies on it.

A CPA letter with inaccurate financial figures produces immediate application rejection when the discrepancy is discovered during underwriting. Lenders cross-reference the figures in the CPA letter against tax returns, bank statements, and IRS transcripts. More significantly, mortgage lenders report fraudulent application activity to the Mortgage Fraud reporting systems maintained by Fannie Mae and Freddie Mac — flagging the applicant for heightened scrutiny on all future mortgage applications.

Submitting a CPA letter with deliberately false financial information in connection with a mortgage application constitutes mortgage fraud under 18 U.S.C. § 1014 — a federal statute prohibiting knowingly making false statements to influence a federally insured financial institution. The FBI and HUD Office of Inspector General actively investigate mortgage fraud cases involving falsified income documentation. Federal mortgage fraud convictions carry penalties of up to 30 years imprisonment and fines of up to $1 million per count.

A CPA who signs a verification letter containing materially false information faces 3 levels of professional consequence: (1) AICPA Ethics Violation — violation of Rule 1.700.001 of the Code of Professional Conduct, potential membership termination, (2) State Board License Action — sanctions ranging from formal reprimand to permanent license revocation, with revocations reported through NASBA's interstate reporting systems affecting all states where the CPA holds licensure, (3) Civil Malpractice Liability — financial exposure potentially reaching the full value of the loan amount for each fraudulent letter.

A CPA letter submitted to USCIS or a U.S. consulate containing materially false financial information produces 3 immigration-specific consequences: (1) Petition denial and bar on refiling — potential permanent bars on certain petition categories, (2) Finding of misrepresentation under INA Section 212(a)(6)(C) — rendering the applicant permanently inadmissible to the United States, barring all future U.S. visas, green cards, and citizenship applications unless a waiver is granted, (3) Criminal charges under 18 U.S.C. § 1546 — up to 10 years imprisonment for standard violations.

The Correct Approach — Professionally Prepared by Tim Martin, CPA

Every Ignition Tax CPA letter is prepared in strict compliance with AICPA professional standards, using only verified financial records reviewed by Tim Martin, CPA. Every letter is prepared to meet the specific requirements of the requesting institution — Fannie Mae, Freddie Mac, FHA, SBA, USCIS, or court — and delivered with the professional accountability that gives lenders, landlords, and government agencies confidence in the verification they receive.

1. Existing vs New Client — Existing tax clients pay 30–50% less at most firms. At Ignition Tax: same $199 regardless.

2. Business Structure Complexity — S-Corp shareholders with multiple K-1s cost more than sole proprietors at hourly-rate firms. At Ignition Tax: same $199 regardless.

3. Geographic Market — CPAs in New York, Los Angeles, and San Francisco charge more. Ignition Tax is national — same $199 everywhere.

4. Rush or Same-Day Turnaround — Most firms add $75–$150 for rush. At Ignition Tax: same $199 — no rush surcharge.

5. Notarization — Adds $25–$75 at most firms. At Ignition Tax: notarized version is $349 flat — a $50 addition only.

Conventional Mortgage — Fannie Mae and Freddie Mac

Freddie Mac requires the letter to be dated within 120 days of the note date for purchase transactions and 120 days of the application date for refinance transactions.

FHA Loans — HUD Handbook 4000.1 FHA lenders apply a 120-day validity window aligned with HUD Handbook 4000.1 requirements.

Landlords and Property Managers Most property managers accept a CPA letter dated within 60–90 days of the rental application submission date.

USCIS and Immigration Authorities Immigration attorneys recommend financial documentation be dated within 6 months of the petition filing date. Courts assess relevance case-by-case.

All letter types, all business structures, all turnaround speeds — $199 standard. $349 notarized. No hidden charges. No hourly billing. No rush surcharge.

CPA Letter for Self Employed or Business owners needs a CPA letter for mortgage lender

CPA Letter Plus for Business Partners, Self Employed Individuals need a CPA letter with Notarization

All PAA questions answered — plus every question buyers ask before ordering.

A CPA letter is a professionally binding document that carries legal weight through the CPA’s licensure, professional accountability, and the AICPA ethical standards that govern its preparation — but it is not a legally binding contract between the signing CPA and the requesting institution. The legal weight derives from 3 sources: (1) the signing CPA assumes professional liability for the accuracy of every statement under AICPA standards, (2) a CPA who knowingly includes false information faces civil malpractice liability and potential federal fraud charges, (3) courts, lenders, and government agencies treat it as credible professional evidence because of the legal consequences the CPA faces for misrepresentation. A CPA letter is not a guarantee, contract, or surety instrument — it provides verified, professionally accountable financial information that the requesting party uses to make their own independent decision.

No. A CPA letter is valid only when signed by a licensed Certified Public Accountant — a professional who holds an active CPA license issued by a state board of accountancy, has passed the Uniform CPA Examination, and meets ongoing continuing professional education requirements. 4 categories of financial professionals cannot issue a legally recognized CPA letter: (1) Bookkeepers — manage financial records but do not hold a CPA license, (2) Tax preparers — PTIN holders including those with IRS Annual Filing Season Program records of completion are not licensed CPAs, (3) Enrolled agents — federally licensed tax practitioners authorized to represent taxpayers before the IRS, but they do not hold a CPA license, (4) Unlicensed accountants — professionals with accounting degrees who have not passed the Uniform CPA Examination. Lenders, USCIS adjudicators, and SBA underwriters verify the signing professional’s CPA license status before accepting the letter.

A CPA letter’s validity period is determined by the requesting institution — not the document itself. The 4 standard validity windows are: (1) Conventional mortgage lenders following Fannie Mae and Freddie Mac guidelines: 120 days, (2) FHA lenders under HUD Handbook 4000.1: 120 days, (3) Most landlords and property managers: 60–90 days, (4) USCIS immigration petitions: 6 months as recommended by immigration attorneys. Courts and legal proceedings do not impose a fixed validity window — relevance is assessed by the presiding judge based on the specific facts of the case. A CPA letter prepared for one application cannot be reused for a subsequent application — each application requires a new letter addressed to the specific requesting institution.

A CPA letter does not require notarization for most domestic applications — including conventional mortgage applications, FHA and VA loan applications, standard rental and lease agreements, and SBA loan submissions. The CPA’s professional license, firm letterhead, license number, and direct contact information provide sufficient authentication for domestic institutional use. Notarization is required or strongly recommended in 4 specific contexts: (1) International visa applications processed through foreign consulates, (2) Certain USCIS immigration petitions specifying notarized supporting documentation, (3) Legal proceedings in jurisdictions requiring notarized financial evidence, (4) International business transactions with parties operating under civil law systems — particularly in continental Europe and Latin America. At Ignition Tax, the notarized version is $349 — a $150 addition to the $199 standard price.

A comfort letter is one specific type of CPA letter — not a separate document category. The term “comfort letter” refers to a CPA verification letter prepared specifically for mortgage lenders, commercial lenders, and third-party financial institutions requesting independent confirmation of a borrower’s income stability and business legitimacy. The CPA comfort letter differs from a standard income verification letter in one defining characteristic — it includes a statement confirming that the CPA has no knowledge of any material changes to the business that would affect the borrower’s income stability at the time of the application. This forward-status confirmation is what gives lenders the “comfort” that the business remains operational beyond the date of the last tax filing. All comfort letters are CPA letters. Not all CPA letters are comfort letters — income verification letters, net worth letters, opinion letters, and letters to management are distinct types serving different verification purposes.

A lender rejects a CPA letter for 5 specific reasons, each with a defined corrective action: (1) Non-licensed signatory — the letter was signed by a non-CPA professional. Fix: obtain a replacement from a licensed CPA whose credentials can be verified through the state board of accountancy. (2) Missing required components — the letter omits information required by the lender’s guidelines. Fix: contact the CPA and request a revised letter addressing the missing components. (3) Letter outside the validity window — the letter is dated outside the lender’s required validity period. Fix: request a new letter dated within the required window. (4) Income figures inconsistent with tax returns — the figures don’t align with filed tax returns. Fix: review the discrepancy with the CPA, identify the source, and resubmit a corrected letter. (5) Incorrect format or addressee — the letter doesn’t follow the lender’s required template. Fix: provide the lender’s requirements to the CPA and request a reissued letter. Most rejection reasons are correctable within 1–2 business days when the applicant has an experienced CPA. Ignition Tax reviews every letter against the requesting institution’s specific requirements before delivery — reducing lender rejection risk to near zero.

Electronically signed CPA letters are accepted by most domestic lenders, landlords, and government agencies in 2026, following the broad institutional adoption of electronic signatures under the Electronic Signatures in Global and National Commerce Act (E-SIGN Act) and the Uniform Electronic Transactions Act (UETA). Fannie Mae and Freddie Mac both accept electronically signed documents in the mortgage origination process, including CPA letters, provided the electronic signature platform complies with their guidelines. FHA and VA loan programs similarly accept electronic signatures on supporting documentation. USCIS accepts electronically prepared and submitted supporting documents for petitions filed through its online filing system. Foreign consulates and embassies have variable electronic signature acceptance policies — physical wet ink signatures with notarization remain the standard for international document submissions in countries that have not formally adopted electronic signature frameworks.

A CPA letter is admissible as financial evidence in civil legal proceedings when submitted through proper evidentiary channels. Courts accept CPA letters as professional financial verification documents in divorce proceedings, child support and alimony calculations, business disputes, partnership dissolutions, and bankruptcy proceedings. The evidentiary weight depends on 3 factors: the qualifications and active license status of the signing CPA, the completeness and accuracy of the financial records the letter is based on, and whether the letter was prepared specifically for the legal proceeding or adapted from a letter prepared for another purpose. Courts may require the signing CPA to testify as an expert witness to authenticate the letter and explain the professional basis for its conclusions. In criminal proceedings, a CPA letter submitted as evidence is subject to the Federal Rules of Evidence and requires authentication through the testimony of the signing CPA or through stipulation between the parties.

A CPA letter is obtained quickly by providing complete financial documents at the time of engagement and selecting a CPA service that offers same-day turnaround. The 3 steps that produce the fastest turnaround: (1) Prepare all required documents before contacting the CPA — incomplete document packages are the primary cause of delays, (2) Confirm the requesting institution’s specific requirements in advance — providing the exact format, addressee information, and content requirements eliminates revision cycles, (3) Select a specialist CPA letter service with same-day capability — general practice CPAs cannot always accommodate same-day requests. Ignition Tax provides a same-day CPA letter service with delivery within 2 hours of receiving complete financial documentation — submit before 12PM EST for guaranteed same-day delivery at $199, no rush surcharge.

A CPA letter and a financial statement are 2 distinct documents serving fundamentally different purposes. A financial statement — including the balance sheet, income statement, and cash flow statement — is a comprehensive summary of a business’s complete financial position prepared according to Generally Accepted Accounting Principles (GAAP). A CPA letter is a targeted verification document confirming specific financial facts — income figures, business operating status, ownership percentage, and tax compliance — drawn from reviewed financial records including tax returns and financial statements. Financial statements are used for internal management decisions, external investor reporting, regulatory compliance, and audit purposes. CPA letters are used for mortgage applications, rental verifications, immigration petitions, SBA loans, and legal proceedings. A financial statement is the underlying record — a CPA letter is the professional verification of specific elements within that record for a specific third-party purpose.

Still have questions?

Now that you know what a CPA letter is — find the specific letter type you need. All $199 standard. All $349 notarized. All delivered in 2 hours.

Income and self-employment verification for mortgage lenders — Fannie Mae aligned

Income confirmation for lenders, landlords, and institutions

Third-party verification for lenders and financial institutions

Self-employment status and income verification — all use cases

Business expense ratio for non-QM bank statement loans

Fast landlord-ready income verification for rental applications

Fannie Mae B3-4.2-01 business fund withdrawal verification

Notarized income verification for visa and immigration applications

2 hour delivery — no rush surcharge — submit before 12PM EST

$199 flat fee. Prepared by Tim Martin, CPA — NY State licensed, AICPA member — and delivered in 2 hours. All letter types. All 50 states. 100% acceptance guarantee.

Need it today? Submit before 12PM EST for same-day fast delivery — 2 hours.

Not sure which letter type you need? Message us on WhatsApp with your situation and we confirm which letter type applies — at no charge