If you are in process of loan & lender requires CPA letter to verify your status, Income or self employment then you are in the right place.

CPA Letter for Self Employed or Business owners needs a CPA letter for mortgage lender

CPA Letter Plus for Business Partners, Self Employed Individuals need a CPA letter with Notarization

Click the "Request" button to place your order easily.

Complete the checkout process to confirm your order.

Fill out the form after checkout and get live portal access.

You are all done, CPA will write your letter in 2 hours.

If you’re business owner, Employed or self-employed and have talked to mortgage lenders, bankers, landlords, renting or buying a home, they might have request you for a letter from your CPA to confirm or estimate your income. Below Find out what CPA letters are and how CPA letter services can help you.

Ignitiontax prepares CPA Letter services for the United States. Scope is clear. We verify income and facts from tax returns, bank statements, and financial statements. We align wording to lender and landlord checklists. For self-employed clients, most mortgage programs expect one to two years of federal tax returns. Fannie Mae and Freddie Mac outline these documentation rules.

We follow AICPA(American Institute of Certified Public Accountants) guidance for third-party verification and comfort letters. We state what was checked. We avoid assurances outside CPA standards.

Banks or lenders require a CPA letter to verify your financials or business status for loan approval.

Prepared for mortgage brokers, banks, and refinancing. We align with agency documentation rules for self-employed borrowers—typically one to two years of signed federal returns, with program variations. We reflect the verified figures and the period covered.

The letter can support: income stability notes, business existence, and source-of-funds or use-of-business-funds confirmation when requested. We coordinate delivery to the lender and include lender name, address, loan number(if provided), and the borrower’s consent.

A CPA writes a letter confirming your earnings for various purposes, ensuring accurate income verification.

For lenders, landlords, and banks. We confirm income using IRS(Internal Revenue Service) tax returns, year-to-date P&L, balance sheet, and bank statements. Letter includes client name, business entity(if any), time in business, method used, and signature on CPA letterhead. Many landlords accept a CPA letter as proof of income along with tax returns and statements.

Use cases: mortgage pre-approval, apartment application, lease renewal, line of credit, and underwriting re-verification. We tailor the cpa letter sample to the recipient’s template when provided.

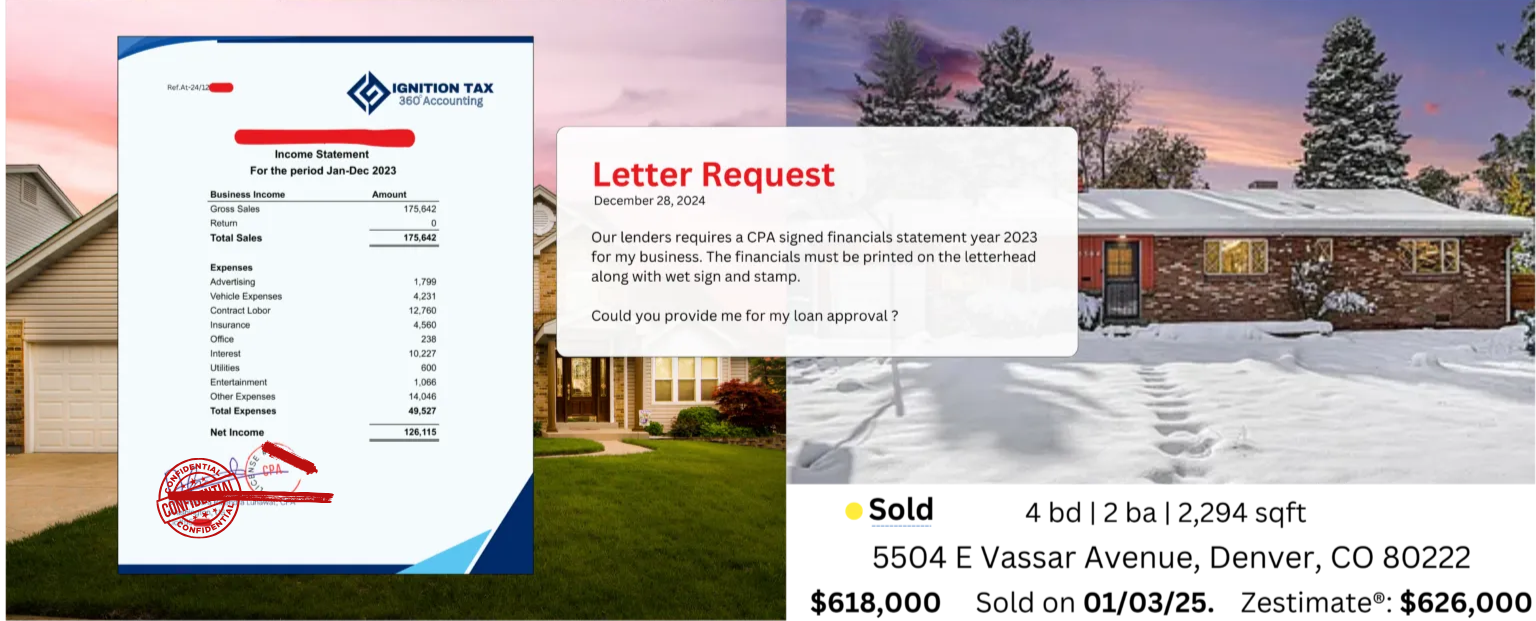

Need to verify your business expense ratio? This letter, requested by lenders or banks, confirms your working expenses.

Some lenders and landlords ask for an expense ratio.

We calculate the expense percentage from your income statement and supporting records.

The letter states the period covered, method used, key components, and limits.

It does not replace audited financial statements. It gives the recipient a concise expense view linked to actual records.

Looking to lease or rent an apartment? A CPA can write a letter verifying your status for tenant or lender needs.

Landlords and property managers want reliable income verification.

We prepare a CPA proof of income letter that pairs with tax returns, bank statements, or a current P&L (profit and loss).

Letters include recipient name, property address if available, period covered, and CPA signature on letterhead. Delivery can go directly to the leasing office upon your consent.

Certify your self-employment status with a CPA letter, ensuring 100% approval for your needs.

This CPA letter is built for sole proprietorship and small business owners. It addresses self-employment income, expense patterns, and business stability.

Most mortgage programs require one to two years of signed federal tax returns for self-employed borrowers. We align the letter with the figures under review.

Self-employment is common. In Q4 2023, 9.1 million unincorporated self-employed workers represented 5.7% of nonagricultural workers. Lenders often need third-party confirmation for this group.

Own a business? A CPA will write a letter confirming your business name, status, and ownership.

Lenders often ask for a “use of funds” confirmation.

We issue a CPA letter that states the intended use: down payment, closing costs, line of credit, equipment purchase, or working capital.

We reference the source of funds and relevant financial records.

We confirm the transaction is recorded within standard accounting practices and consistent with the business purpose.

If policy language is required, we align wording to the lender’s checklist and program rules.

This letter supports underwriting for business loan, line of credit, mortgage, or refinancing.

We include recipient name, loan number(if provided), period covered, and CPA signature.

When requested, we add a brief statement on solvency indicators tied to financial statements—without providing an audit opinion.

A CPA can write a letter to meet your unique needs, whether legal, professional, or other purposes.

We start every project with a CPA engagement letter.

It defines scope, deliverables, timeline, and fees.

It explains responsibilities: client, lender, and CPA.

It covers confidentiality, data access, and record retention.

It states liability (financial accounting) limits and indemnity terms.

It references applicable standards: AICPA(American Institute of Certified Public Accountants) and state board rules.

You receive clear terms before work begins—no surprises.

Use cases: income verification, CPA comfort letter, CPA 3rd party verification, CPA expense ratio letter, and CPA letter of explanation.

Entities included: client name, business entity, recipient, purpose, and consent for third-party delivery.

We reference documents examined and calculations made. We do not provide an audit opinion or guarantee loan performance.

We explain procedures performed and the limits of our work. We reference documents examined and calculations made. We do not provide an audit opinion or guarantee loan performance. Our language follows AICPA comfort-letter guidance and third-party verification practices to reduce misinterpretation and risk.

Common requests: confirmation of self-employment, business existence, revenue methods, and expense ratio notes. When a requester asks for assertions beyond CPA standards, we propose acceptable wording instead.

A CPA can write a letter to meet your unique needs, whether legal, professional, or other purposes.

We issue a CPA verification letter to third parties. Banks, insurance carriers, mortgage brokers, and creditors use it to confirm facts.

Scope is defined. We confirm items we can support with tax returns, financial statements, and bank statements.

Typical requests: self-employment status, time in business, business existence, revenue method, and use of business funds.

Language follows AICPA(American Institute of Certified Public Accountants) guidance for comfort letters and third-party verifications. We explain procedures and limits to avoid misinterpretation.

A CPA can write a letter to meet your unique needs, whether legal, professional, or other purposes.

Underwriting flags unusual items. We provide a CPA letter of explanation to add context.

Use cases: large year-over-year changes, seasonal revenue, one-time expenses, or a recent entity change.

We reference source documents and calculations. We avoid legal advice.

Our goal is clarity for credit risk review and a direct link to the loan file.

Your letter appears on CPA letterhead with signature, seal, and notarial acknowledgment. We confirm identity, date, and capacity.

Some recipients require a notarized CPA letter.

This occurs with certain state forms, lenders, and adoption or immigration files.

We coordinate a commissioned notary.

Your letter appears on CPA letterhead with signature, seal, and notarial acknowledgment.

We confirm identity, date, and capacity.

Scope remains the same: we verify facts from tax returns, financial statements, and bank statements.

We do not provide legal advice.

Common requests: mortgage packages, apartment rentals, business licenses, insurance, and creditor files.

Ask for a notarized option when the checklist mentions “notary,” “acknowledgment,” or “jurat.”

This letter, required by lenders or tenants, certifies your employment status, tenure, and wages.

A CPA letter for a mortgage verifies a borrower’s financial information. This letter is mostly requested by lenders to confirm the accuracy of an individual’s income, assets, and financial health at the time of applying for a mortgage loan.

A CPA Letter confirms an individual’s or Business income at the time of applying for loans, mortgages, or rental properties. It is requested by the lender to verify the applicant’s monthly or yearly income. This sort of letter assures the lender about the repayment of the loan. Mostly requested for self-employed individuals or those with irregular income streams.

A CPA letter to certify an applicant individual’s self-employment status and income. This letter is mostly requested by lenders and landlords. The main purpose is to assure the income and the stability of a self-employed person’s business.

It is a letter provided by a Certified Public Accountant (CPA) to verify a tenant’s financial status, usually required by landlords or property managers during the rental application process. This letter confirms the tenant’s income, employment status, etc.

A CPA comfort letter that confirms certain financial or accounting positions of an individual or business. It is used in multiple situations, such as at the time of mortgage loan, Yearly audits, or during business transactions. The letter offers a level of comfort and assurance to third parties, typically lenders or investors, by providing a validation of financial information.

A CPA letter for the withdrawal of business funds is a statement that CPA mentioned on the letter along with the business details. The purpose of this letter confirms to the lender that withdrawal of funds from a business will not negatively affect the business operations or stability.

A CPA letter for the use of business funds is also a statement that certifies the bank or lender that use of business funds will not harm or affect the business.

A CPA letter is required by lenders or other third parties to confirm the accuracy of financials of a borrower or client, especially when applying for loans, mortgages, or other financial transactions.

A CPA letter to validate the accuracy and completeness of a client’s financial statements, such as profit and loss statements and balance sheets. This letter is required for businesses seeking to reassure investors, lenders, or other stakeholders of the reliability of their financial records.

A CPA letter confirms an individual’s employment status and income. This letter is commonly requested by employers, lenders, or other entities that need to verify a person’s employment status and income level.

A CPA letter of business existence is an official document issued by a Certified Public Accountant (CPA) that confirms the existence and operational status of a business. CPA verifying the business name, address, ownership on the letterhead. It can be requested by banks, lenders, or other entities to verify that a business is legally registered and active on the location.

A CPA letter verifies and details a business’s assets. It’s commonly needed for securing loans, attracting investors, or during mergers and acquisitions. The letter confirms the value and existence of assets like equipment, inventory, real estate, and intellectual property.

While every CPA letter is unique, most of the letters include the details like Name, Address, Business nature of the applicant.

A valid CPA letterhead contains the details like name, address, License,Company Logo of the active Certified Public Accountant.

It includes the full legal name of the Person who is requesting this letter.

The details of the business are required to be mentioned on the CPA letterhead to Certify the business, Income, ownership percentage, etc.

In the case of Sole Proprietor, applicant name and address will be mentioned on the letter.

The contact of the applicant is to be mentioned on the letterhead to keep in record of the Certified Public Accountant and third party.

Percentage of ownership shows how much of a company or asset someone owns. It indicates their share of control over the company’s equity, usually given as a percentage of the total.

Example: Emily owns 40% of a small tech startup, meaning she has a 40% stake in the company. This percentage gives her a corresponding share of the company’s profits, voting rights, etc.

The CPA letters describe the nature of a business, what a company does and its primary activities. It outlines the core operations, products, or services that define the business.

Example: A bakery’s nature of business is to bake and sell fresh bread and pastries, serving local customers with a focus on high-quality, homemade baked goods.

The CPA letter should include the exact number of years or the date since the applicant has been working or owned the business.

Example: Mr. John Doe Smith has been in business as the sole proprietor since 07, July 2021.

The lender requested the applicant to provide a letter to verify the Employment status and Income of the Applicant.

Example: Mr. David worked as Director of Finance at Abc Marketing, Inc.

This statement is requested by the lender to specify from how long the CPA has been preparing the applicant’s tax returns.

Example: Mr. Eric Holland, CPA has prepared and Filed the tax return of “Applicant” for the year 2023..

This statement on CPA letters is requested by the lender at the time of loan process. It verifies that CPA has reviewed the Financials or Tax Return of the applicant.

CPA letter must have a signature from Licensed CPA whether independent or working for an accountancy firm.

The letter can not be considered as validated until the CPA complete name, Licence number and address mentioned on the letter.

A CPA letter is a document from a Certified Public Accountant that confirms your financial status or details. It’s often needed to reassure lenders or landlords about your financial reliability..

A CPA letter costs $199 for basic letter and $249 for letter plus. Both options include unlimited revisions until your loan is approved.

It covers income verification, self-employment status, and ownership percentage. For business partners, it also includes financial statement verification and details on how business funds are used.

After placing order, you’ll recieve your letter in 2 to 3 hours.

Lenders use CPA letters to verify that you have a stable income and are financially sound enough to repay a loan.

You can get a CPA letter from your current CPA or through Ignition Tax CPA’s. They can provide the verification you need based on your financial documents.

A CPA letter for mortgage can be the difference between delay and decision on your home loan.

Mortgage lenders want clear income verification. They want proof that your earnings are consistent, tax compliant, and well documented.

Ignition Tax prepares lender-ready CPA letters that explain your income, your business activity, and your financial health in simple terms.

This helps your mortgage lender read your file faster and see how you qualify for the mortgage loan you need.

Buying or refinancing a home in Brooklyn usually means detailed questions from your mortgage lender.

This is especially true if you are self employed, own an LLC, or have several income streams.

Most lenders rely on tax returns, financial statements, and bank statements to assess risk.

When income is complex, they often ask for a CPA letter for mortgage to confirm income stability, tax compliance, and business ownership.

Ignition Tax is a certified public accountant (CPA) and accounting firm serving Brooklyn, NY.

We focus on CPA letters for mortgage lenders, home loans, and refinance requests for self-employed borrowers and small business owners.

Your CPA mortgage letter from Ignition Tax is written on official CPA letterhead.

It summarises your income, verifies your business activity, and supports your mortgage approval process in a clear, direct way.

If you need a CPA letter for mortgage in Brooklyn, you can contact Ignition Tax to start the income verification review today.

Each CPA mortgage letter is prepared to match what mortgage lenders look for in an income verification document.

We focus on clarity, consistency, and tax compliance, so your lender can read and understand your financial position without confusion.

Our team at Ignition Tax reviews your tax returns, financial statements, and business activity before we sign your CPA letter for mortgage.

This helps your mortgage lender see how your income supports the home loan you are applying for in Brooklyn, NY.

If your lender has asked for a CPA letter, you do not need to guess what to do next.

You can get CPA letter for mortgage support from Ignition Tax with a simple call or short form.

Contact us to schedule a quick consultation, share your loan details, and start your income verification review.

Whether you searched for “CPA letter for mortgage near me” or specifically “CPA letter for mortgage Brooklyn NY”, Ignition Tax is ready to help you move your mortgage application forward.

A CPA letter for mortgage is a written statement from a certified public accountant.

It confirms key details about your income, your business activity, and your tax position.

Some lenders call it a CPA Mortgage letter or a CPA letter to lender.

All of these phrases point to the same thing.

A signed document on CPA letterhead that supports your loan application and shows how you earn your money.

Mortgage lenders use this letter during a mortgage loan, home mortgage, refinance, or first home loan review.

It helps the lender, mortgage lender, mortgage company, or money lender understand your numbers when they are not simple W-2 wages.

In many files, income is the part that raises the most questions.

Industry reports often show that income documentation and tax issues are among the most common reasons for mortgage delays.

A clear CPA letter for mortgage can reduce these questions by explaining how your income works over time.

The letter supports income verification.

It can confirm that your income is real, that it comes from a legal source, and that the level of income is consistent with your tax returns and bank statements.

It also supports tax compliance.

The CPA confirms that the income has been reported to the IRS under current tax law, or explains any items that need extra context.

Finally, the letter gives a short picture of your financial health and sometimes touches on credit history, assets, or ownership structure if needed.

This helps the lender judge risk, set terms, and decide if the mortgage can be approved.

A certified public accountant does more than sign a form.

They act as a neutral financial professional who understands your numbers and the rules that apply to them.

As a public accountant, tax consultant, and financial consultant, the CPA reviews your records before issuing the letter.

This can include bank statements, tax returns, financial statements, and business ownership documents.

The goal is accuracy.

The CPA checks that the information in the letter matches your tax filings and your real income.

This is important because lenders rely on that verification when they decide whether to approve your mortgage loan or home mortgage.

A strong CPA letter often explains:

The CPA must also think about IRS rules, tax law, and professional compliance.

They cannot say more than the documents support.

This keeps the letter honest and reliable for both you and the lender.

When Ignition Tax issues a CPA letter for mortgage, the focus is clear.

We make sure the content is accurate, supported by records, and written in a way that a mortgage underwriter can understand quickly.

Not every borrower needs a CPA letter.

Lenders usually ask for it when income is complex or not shown on a simple paycheck.

Common situations include self-employment and sole proprietors.

If you file Schedule-C or report business income on your personal return, a lender may want a CPA verification letter for mortgage to confirm how that income is calculated.

LLC owners often face the same request.

Income can pass through to the owners in different ways.

A CPA letter can explain the ownership, the income share, and how stable that income is from year to year.

Borrowers who work with the Small Business Administration (SBA), or who own several small businesses, may also be asked for a CPA verification of income for mortgage.

Lenders want to see that a qualified professional has reviewed the numbers.

Real estate investors and landlords are another group that often hear this request.

Rental income can come from several properties and entities.

A CPA can show how much of that income really belongs to the borrower and how it appears in tax filings.

Finally, gig workers, contractors, and people with several side income streams may be asked for a CPA written verification for mortgage.

Platforms may not issue traditional pay stubs.

The CPA letter links bank deposits, tax returns, and actual earnings into one clear explanation for the lender.

In all these cases, Ignition Tax can prepare a CPA letter for mortgage that fits your situation.

The goal is simple.

Help the lender understand your income so you can move your application forward with less stress and fewer delays.

A CPA letter for mortgage is more than a form.

It is a focused tool that supports your home loan request and answers your lender’s main questions.

Ignition Tax prepares each letter with your income pattern, tax filings, and business structure in mind.

This gives your lender a clear view of your income, your self-employment, and your financial position in Brooklyn, NY.

If you are self employed, your income often looks different each year.

A CPA letter for self employed mortgage explains how your self-employment income works over time.

We review your Schedule-C, business income, and related financial statements before we sign anything.

The letter can:

This becomes a CPA income verification letter for mortgage that ties your tax returns, your bank activity, and your business story together.

For many self-employed borrowers, this extra clarity can make the mortgage underwriter more comfortable with the file.

Underwriters work under strict rules.

They must understand every key number in your loan application before they approve a mortgage loan.

A CPA letter from Ignition Tax supports this underwriting process.

It acts like a focused application letter that speaks directly to the financial questions in your file.

We prepare the letter as part of your document verification package.

It can be used during a mortgage review, or paired with a mortgage comfort letter or lender comfort letter, depending on what your mortgage lender requests.

The focus is on:

When the information is easy to read and internally consistent, the lender usually asks fewer follow-up questions.

That can mean less back-and-forth for you and a smoother path to a decision.

Lenders look at more than income.

They also review credit history, cash flow, and tax records to understand the risk of each borrower.

A CPA letter can address these areas when needed.

Ignition Tax can reference your bank statements, key assets, and financial statements to give context that may not be obvious from numbers alone.

For example, the letter can explain:

This added detail helps the lender see why your numbers look the way they do.

It gives a more complete picture of you as an applicant, not just a set of forms.

Many files slow down because lenders cannot easily verify income.

A clear CPA letter for mortgage approval can limit these delays.

It pulls the key points together and shows how your income supports the mortgage amount you are seeking.

Ignition Tax also focuses on tax compliance and accurate reporting.

When the letter confirms that income ties back to tax filings and proper records, lenders gain more confidence.

In many cases, a well-structured CPA letter confirming income for mortgage reduces the back-and-forth between you and the lender.

This does not guarantee approval, but it can help the lender reach a decision sooner and with fewer obstacles.

Ignition Tax focuses on CPA letters that speak directly to what lenders in Brooklyn, NY need to see.

Our work covers letters to mortgage lenders, banks, credit unions, and other money lenders reviewing your mortgage loans, home loan, or refinance request.

We support self-employed borrowers, LLC owners, landlords, and real estate investors.

Each CPA letter for mortgage is prepared based on your records, your tax history, and your specific lender request.

Many borrowers hear about a “CPA letter to mortgage lender” only after the lender asks for one.

This usually happens when income is not simple salary or when the lender wants extra comfort on your financial picture.

Ignition Tax prepares CPA letters for:

Your letter can be addressed as a CPA letter to bank for mortgage or a CPA letter to a specific mortgage lender.

When required, we can also structure the content as a CPA comfort letter to lenders, focused on the lender’s risk questions.

Each letter is built around:

This helps the lender link your income and tax data to the mortgage terms they are considering.

Self-employed borrowers often face more questions during mortgage review.

Lenders want to see how business income is earned, how stable it is, and how long the business has been active.

Ignition Tax can prepare a CPA letter for mortgage loan that explains your self-employment clearly.

When useful, we can also align our content with a CPA letter for self employed mortgage template, customized to your lender’s checklist.

We work with:

As an accounting firm and business management consultant, we understand how lenders interpret business income.

Your CPA letter will connect your business records, tax filings, and income trends in a way that supports your mortgage file.

This gives the lender a clear explanation of your role, your income sources, and the stability of your self-employment.

If you are a landlord or real estate investor, your income may come from several properties and entities.

Ignition Tax prepares CPA letters for:

In these cases, the CPA letter can summarize your rental income, key assets, and overall financial health related to the properties.

It can explain how rental income appears in your tax returns and how it flows through to you as the borrower.

Some lenders also request a CPA mortgage letter request for solvency.

In that situation, we focus on whether the entity or property portfolio can meet its obligations based on current income and expenses.

This added explanation helps lenders see how your real estate activity supports the home loan or mortgage loan you are applying for, especially when the file includes several properties, loans, and cash flows.

When a lender asks for a CPA letter, most borrowers want two things.

They want the letter done correctly.

And they want it accepted without repeated edits or new drafts.

Ignition Tax focuses on CPA mortgage letters for Brooklyn homebuyers and real estate owners.

We match lender requirements with your real financial records so the letter supports your mortgage file in a clear, direct way.

Ignition Tax is led by a certified public accountant who understands how lenders read income.

Our work includes tax preparation, financial statements, and mortgage-related documentation.

When we issue a CPA letter for mortgage, we do it under strict professional standards.

We carry professional liability coverage and errors and omissions protection, supported by proper liability insurance.

This matters to many mortgage lenders, because it shows that a licensed professional is taking responsibility for the content.

Our focus is on mortgage lender requirements.

We look at what your underwriter has asked for.

Then we prepare the CPA letter so it stays within professional rules and still answers key income and tax questions.

Many lenders expect a specific CPA letter format for mortgage files.

They want clear headings, simple statements, and easy ways to contact the CPA if they have questions.

Ignition Tax prepares each letter on formal CPA letterhead.

The letter includes:

If your lender shared a CPA letter for mortgage sample or a preferred layout, we can follow that structure where it fits professional standards.

We can also base your letter on a CPA letter for mortgage template that reflects common lender expectations while still being tailored to your own numbers.

This helps underwriters review your letter quickly, without having to guess who signed it or what documents were used.

Many borrowers worry about the CPA letter for mortgage cost.

They are already dealing with closing costs, appraisal fees, and other charges.

Ignition Tax uses a simple and transparent approach to pricing.

We explain the fee for your CPA letter before we start the review.

If extra work is needed, such as additional tax analysis or updated financial statements, we tell you in advance.

There are no hidden charges or surprise add-ons after the letter is complete.

You know what you are paying for.

Review of your records, preparation of the CPA letter, and, if needed, limited follow-up answers to lender questions about that letter.

A Brooklyn CPA letter for mortgage often involves local lenders, regional banks, and New York based mortgage companies.

Each has its own way of asking for documentation.

Ignition Tax works with borrowers across Brooklyn, NY.

We see the patterns in what lenders request for Brooklyn NY CPA letter for mortgage files.

Common requests include clarity on self-employment income, rental income from local properties, and multi-owner LLCs that hold Brooklyn real estate.

This local experience helps us shape a Brooklyn New York CPA letter for mortgage that fits the type of review your lender is doing.

We understand common documentation expectations, such as:

By combining local insight with solid CPA work, Ignition Tax aims to make your CPA mortgage letter easier for Brooklyn lenders to understand and process.

Ignition Tax follows a clear process for every CPA letter for mortgage.

Each step connects your real numbers to what your lender needs for your mortgage loan or home mortgage.

We start with your loan application.

Your lender has already asked for certain documents and raised specific questions.

As the applicant, you share the key items linked to your mortgage loan or home mortgage review.

This is similar to preparing a focused job application, but centered on your income and tax records.

Typical documents include:

These records help us see how your income appears on paper before we prepare any CPA letter.

Next, we review your financial statements and prior tax preparation work.

If Ignition Tax already handles your tax preparation services, we build on that existing knowledge.

If another firm prepared your returns, we still check the filings and supporting documents.

When needed, we may recommend a limited financial audit style review, just enough to confirm key numbers for the letter.

We also consider the perspective of a tax assessor and the lender’s underwriter.

The focus is on:

Only after this review do we move on to drafting the CPA letter.

Once we understand your numbers, we prepare the draft CPA Mortgage letter.

This document is designed for your specific lender or CPA letter for mortgage company request.

The draft functions as a focused CPA verification letter for mortgage.

It explains your income, your business, and your tax position in simple, direct language.

While drafting, we make sure the wording:

We do not promise future income or make unsupported statements.

We only confirm what your records and filings can support.

If needed, the draft can be reviewed by the lender or loan officer for format questions before final sign-off, without changing the underlying facts.

After the draft is confirmed, we issue the final CPA letter on official Ignition Tax letterhead.

The letter is certified by a licensed CPA and formally signed.

This final version includes:

We can deliver the final letter as:

Throughout this stage, we maintain credibility, accuracy, and proper verification standards.

Our work is backed by professional liability coverage and internal quality checks, so your CPA letter for mortgage is ready to be used in your loan file.

Your CPA letter for mortgage often connects with other support services.

Ignition Tax offers related documents and reviews that can help strengthen your full mortgage file.

These sub-services are optional but can be useful when lenders ask for extra comfort, more detail, or updated financial information.

Some lenders go beyond a simple income letter.

They may ask for a CPA comfort letter for mortgage to help them understand specific risk points.

In these situations, Ignition Tax can prepare:

These letters can address topics like business stability, length of operation, or how income trends over time.

They do not guarantee future performance, but they give lenders a clearer picture of your current position, based on records and tax filings.

Not every lender uses the phrase “CPA letter.”

Some lenders ask for an accountant letter for mortgage or an accountant mortgage reference letter instead.

Ignition Tax prepares these letters in line with professional rules.

We can provide:

In each case, the content stays grounded in your real numbers.

We draw from tax returns, financial statements, and other documents to present information the lender can rely on.

Some lenders prefer a more formal style of statement.

They may ask for a CPA certification letter for mortgage that clearly states what has been reviewed.

Ignition Tax can issue:

These letters outline the scope of the review.

They state which documents were considered and what period they cover.

This extra detail helps the lender understand how the CPA reached the stated figures.

When you seek a refinance, lenders may take a closer look at solvency, assets, and liabilities.

They want to see overall financial health, not just current income.

Ignition Tax can assist with:

In these cases, the letter may focus more on balance sheet items and debt coverage.

It connects your assets, liabilities, and income into one clear explanation for the lender.

Many mortgage questions trace back to tax filings and business decisions.

Ignition Tax supports borrowers with ongoing services beyond the CPA letter itself.

We offer:

By aligning your tax strategy, business records, and financial reporting, we help make your profile easier for lenders to understand.

That can support your current mortgage application and future financing plans.

These short case studies show how a focused CPA letter for mortgage can support real situations in Brooklyn.

Details are simplified and anonymized, but the patterns are common for many borrowers we work with.

A self employed web designer in Brooklyn applied for a home loan.

Their income came from many small clients, with busy and slow months.

Ignition Tax reviewed two years of Schedule-C filings, bank deposits, and simple financial summaries.

We prepared a CPA letter explaining:

With this explanation, the lender could see that net income had been consistent over time.

The CPA letter supported the mortgage underwriter’s review and helped the borrower move forward toward buying their home.

A small business owner held their operations through an LLC.

They wanted to refinance an existing mortgage on a Brooklyn property to lower the payment.

The lender asked for more detail on how the business income supported personal cash flow.

They also wanted a clearer picture of assets and liabilities linked to the LLC.

Ignition Tax gathered the LLC financial statements and tax returns.

We prepared a CPA letter that:

The lender used this explanation to understand the overall financial position.

With better insight into income and debt, the refinance review could continue without repeated document requests.

A Brooklyn real estate investor owned several rental units across the borough.

As one of the landlords with multiple properties, they had complex rental income flows and different loan terms on each building.

The lender requested more detail before approving a new mortgage.

They wanted to see if the rental portfolio supported the new payment.

Ignition Tax reviewed property-level financial statements, rent rolls, and tax returns.

We focused on tax compliance, reported rental income, and key expenses.

The CPA letter:

With that clarity, the lender could separate property income from personal income and complete the risk review.

The investor was then able to proceed with the new financing plan for the Brooklyn property.

Feedback from real clients shows how a CPA letter for mortgage can support a loan file.

Ignition Tax focuses on clear communication, reliable numbers, and practical help for Brooklyn borrowers.

Many local homebuyers search for “ignitiontax CPA letter for mortgage reviews” when their lender first asks for a CPA letter.

They want to know how other Brooklyn clients handled the same request.

Clients often mention that Ignition Tax:

Borrowers in ignitiontax Brooklyn cases include self-employed professionals, small business owners, and real estate investors.

In their feedback, they focus on reduced confusion, fewer document gaps, and better understanding of what the lender needed from the CPA.

These experiences show how a focused CPA letter for mortgage can make a complex file easier for both the borrower and the lender.

A large part of our work involves self-employment and small businesses.

Many clients are sole proprietors, LLC owners, or small firms that work with the Small Business Administration.

Ignition Tax helps these business owners by turning their records into clear, lender-ready explanations.

The CPA letter links tax filings, business performance, and income stability in a way underwriters can follow.

Client comments often highlight the relief of having a single document that addresses the lender’s questions.

This does not change the numbers, but it helps lenders see how the business supports the mortgage application.

Lenders must manage risk in every mortgage file.

They look for documentation that is accurate, consistent, and easy to verify.

Ignition Tax prepares CPA mortgage letters that fit these needs.

We focus on documented facts, clear explanations, and alignment with tax records and lender guidelines.

A CPA letter for mortgage is only useful if it is accurate.

Ignition Tax checks your records against IRS filings and current tax law before issuing the letter.

We focus on:

Our work is supported by professional liability coverage and errors and omissions insurance.

This structure encourages careful review and responsible wording in every letter.

By grounding each statement in documents and filings, we help lenders rely on the letter as a stable part of the file.

A CPA letter for mortgage should add value to your file, not create new questions.

Ignition Tax writes each letter with the lender’s review process in mind.

We consider the CPA letter for mortgage review stage.

Underwriters need to see how income, tax returns, and bank statements connect.

Our letter helps link these pieces together.

By providing a clear statement of income, business activity, and tax compliance, the letter supports your CPA letter for mortgage approval goal.

It does not guarantee approval, but it can make it easier for the lender to reach a decision based on complete information.

This lender-focused approach can reduce back-and-forth, shorten review time, and create a more organized document package.

Many borrowers search online for the “best cpa letter for mortgage”.

In practice, the most effective letter is not about big claims.

It is about how well the letter fits your specific situation and your lender’s requirements.

Key factors to consider include:

Ignition Tax structures each CPA letter around these points.

The goal is a document that is clear, well scoped, and backed by real verification, so lenders can rely on it as part of your mortgage review.

Brooklyn borrowers face a mix of high housing costs, complex income, and detailed lender reviews.

A clear CPA letter for mortgage can help lenders read that picture with fewer doubts.

Brooklyn’s home values tend to be higher than the local average income, which can influence mortgage planning.

That makes every number in your file more important.

Lenders look closely at:

If your income is variable or tied to a business, these numbers may not be straightforward.

A CPA letter can explain how income is calculated, how expenses affect net income, and why your debt-to-income ratio still fits the lender’s rules.

Ignition Tax uses your tax returns and financial records to present a simple, lender-ready explanation.

This helps underwriters see how your income supports the payment for a Brooklyn property.

Brooklyn has many self employed professionals, gig workers, and freelancers.

Some also act as small real estate investors on the side.

Platform payments, project-based work, and rental income do not always fit traditional payroll formats.

A CPA letter can:

Ignition Tax reviews gig income, freelance contracts, and rental records and then explains them in a way lenders can follow.

This helps your non-traditional income become easier for underwriters to assess.

Many local lenders have detailed documentation checklists.

They often request a CPA letter for mortgage in Brooklyn when they see self-employment, rental income, or small business ownership.

Ignition Tax responds by aligning the letter with those local expectations.

We look at what your lender has asked for and prepare a response that fits both their needs and professional rules for CPAs.

Whether you found us by searching “CPA letter for mortgage near Brooklyn NY” or through your loan officer, the process is the same.

We connect your documents, tax filings, and business structure into one clear CPA letter that supports your Brooklyn mortgage file.

Sometimes lenders ask for a CPA letter late in the process.

This can feel urgent, especially when closing dates are near.

A little preparation can make that request easier to handle.

Even before you apply, it helps to have your main documents organized.

This makes it faster to prepare a CPA letter when the lender asks.

Key items include:

With these documents ready, Ignition Tax can move from review to draft more efficiently.

Your lender then receives a CPA letter that matches the numbers they already see in your file.

If you need quick help and search for “CPA letter for mortgage near me” or “CPA letter for mortgage near Brooklyn New York”, timing is usually the main concern.

To speed up CPA income verification:

When we have complete information at the start, we can move faster without repeated document requests.

A last-minute request can be stressful, but there is a simple way to respond.

Use this quick checklist:

By following these steps, you can respond to a last-minute CPA letter request in an organized way.

Ignition Tax then focuses on preparing a clear, accurate letter that fits your mortgage file and supports the lender’s review.

Income verification is central to every mortgage review.

Lenders need to see where your income comes from, how stable it is, and how it appears in your tax records.

For borrowers with self-employment, business income, or multiple revenue streams, these checks can feel complex.

A CPA letter for mortgage helps connect the documents into a clearer story for the lender.

When income is based on self-employment, lenders do not rely on a single pay stub.

They look at your tax filings and your business performance over time.

Key points they review include:

Lenders compare these figures to the amount of the mortgage loan you are seeking.

They want to see that your self-employment income is stable enough to support the payment.

A CPA letter for mortgage can explain how the business earns money, how expenses are handled, and how income is calculated from the tax filings.

This makes the self-employment profile easier for an underwriter to evaluate.

Three document types are central to most mortgage files.

Lenders use these documents for verification.

They check that income on the application matches what appears in tax returns and bank statements.

A CPA letter can reference these financial statements, tax returns, and bank statements to show how they tie together.

This helps underwriters see that the numbers are consistent and based on real records.

During review, lenders look for warning signs or missing information.

Examples include:

A CPA letter for mortgage helps by focusing on credibility, accuracy, and compliance.

For example, the letter can:

While the CPA cannot remove risk, they can provide a clear, professional explanation.

This makes it easier for the lender to decide based on complete information rather than uncertainty.

Lenders often have preferences for how a CPA letter should look.

A format that is simple, structured, and easy to scan is usually easier for underwriters to use.

Many borrowers search for a sample CPA letter for mortgage to understand what will be included.

The exact text must match your situation, but the structure is typically similar.

A standard letter template or CPA letter for mortgage template will often include:

Ignition Tax uses this type of layout as a starting point.

We then adjust the content so your CPA letter for mortgage sample is not generic, but tailored to your income and lender request.

Some lenders prefer a more narrative approach.

They ask for a CPA cover letter, an accountant cover letter, or an application letter that accompanies other forms.

In these cases, Ignition Tax can frame the CPA letter as a cover note.

The language is still clear and factual, but it may:

This structure makes it easy for the lender to connect the CPA letter to the rest of the mortgage file.

The tone remains professional and focused on documented facts.

A CPA letter for mortgage versus other documents plays a specific role.

It does not replace standard forms like W-2s or pay stubs, but it adds context where needed.

Comparison points:

The CPA letter sits beside these documents.

It helps lenders connect the dots between raw data and a real, understandable income story.

For many self-employed or complex borrowers, this extra clarity can make the mortgage review process more efficient and less confusing.

Your CPA letter for mortgage is only one part of your financial picture.

Ignition Tax also provides ongoing tax and accounting support that can help keep your records clear for future loans and reviews.

Ignition Tax offers tax preparation service for both individuals and business owners in Brooklyn.

We prepare and file returns that match your real income, deductions, and business activity.

Our tax preparation services include:

Accurate tax preparation makes later income verification easier.

It keeps your mortgage documents, bank statements, and tax filings aligned.

Many borrowers are also business owners.

Ignition Tax supports them as a business management consultant.

We help you review:

These reviews can guide everyday decisions and future planning.

They also help you understand how your business will appear to lenders when you apply for a mortgage or refinance.

Some situations require deeper review or planning.

Ignition Tax can assist with focused financial audit style work when you need more detailed checks of selected records.

We also provide services as a tax consultant, including:

Ongoing compliance support helps keep your books, returns, and documentation consistent.

This reduces surprises when lenders, investors, or agencies ask for records in the future.

Ignition Tax serves borrowers who live, work, or invest in Brooklyn and nearby parts of New York.

Our CPA letters for mortgage are prepared with local lender expectations in mind.

If you search for a Brooklyn CPA letter for mortgage, you are likely working with a local lender or buying in the borough.

Ignition Tax supports clients across Brooklyn, including many of its main neighborhoods.

We provide:

Each letter is based on your actual records and tailored to your lender’s request.

Some clients live outside Brooklyn but work or invest in the area.

If you searched for “CPA letter for mortgage near Brooklyn”, you may need a local CPA who understands the Brooklyn and New York market.

Ignition Tax can help borrowers who need:

We work with you remotely or in person, depending on what fits your situation and timing.

Ignition Tax is a local firm with a certified public accountant leading the work on mortgage-related letters.

If you are looking for “ignitiontax certified public accountant”, you are in the right place.

We focus on ignitiontax CPA letter for mortgage services that support:

By combining local knowledge with clear documentation, we help you present your income and tax records in a way lenders can understand and use in their review.

These answers focus on what self employed borrowers, small business owners, and real estate investors most often ask about CPA letters for mortgage loans.

Not every self employed borrower needs a CPA letter.

It depends on the lender, the mortgage loan program, and how your self-employment income appears in your documents.

Some lenders are satisfied with tax returns, bank statements, and standard forms.

Others ask for a CPA letter when income is hard to read or when they want extra clarity on your business.

You are more likely to need a CPA letter if:

If your lender has questions about how your self-employment supports the loan, a CPA letter for mortgage can help organize the information in a clear way.

A CPA income verification letter focuses on key facts.

It usually includes:

Ignition Tax aims for accuracy in each statement.

We base the letter on tax returns, financial statements, and other records.

The letter is designed for verification.

It does not guarantee future income.

Instead, it confirms what the CPA has seen in your records and explains that information for the lender in simple terms.

Timing depends on how prepared your documents are.

Most of the work happens before the letter is drafted.

To start, we need:

The general steps are:

If your records are complete and organized, the process is usually faster.

When you contact Ignition Tax, we can outline the expected timing based on your specific situation and lender request.

Yes, in many cases we can still help.

Ignition Tax can:

Sometimes this support is used for a new application with the same lender.

In other cases, it helps when you apply with a different lender or explore refinance options later.

We cannot reverse a decision, but we can help you present your information more clearly in the next review.

A CPA letter for mortgage is not required by the IRS.

The IRS focuses on tax returns, payments, and tax law compliance.

The request for a CPA letter comes from mortgage lenders, not from tax authorities.

Lenders use the letter to help them understand your income and risk level for the loan.

So, the roles are different:

A CPA letter connects these two areas by explaining how your taxed income supports the loan you are requesting.

When your lender asks for a CPA letter, taking clear, simple action helps keep your file moving.

Ignition Tax is ready to review your records and prepare a letter that speaks directly to your lender’s needs.

If your lender has asked for a CPA letter, you can reach out now and start the process.

Contact Ignition Tax to:

You can call, send a message, or book a time to talk.

Once we see your documents and your lender’s request, we guide you through each step until the letter is ready.

A clear CPA letter can support your home loan or home mortgage by organizing your income story in one place.

For many borrowers, this income verification step is crucial to moving from application to approval.

If you need a CPA letter for mortgage, you do not have to navigate it alone.

Ignition Tax can review your records, prepare the letter, and help you respond to your lender’s documentation requirements in a structured way.

Reach out to begin your CPA income verification process and take the next step toward your home loan in Brooklyn.